Diamond Market, Week 9, 2026

23 February to 2 March 2026

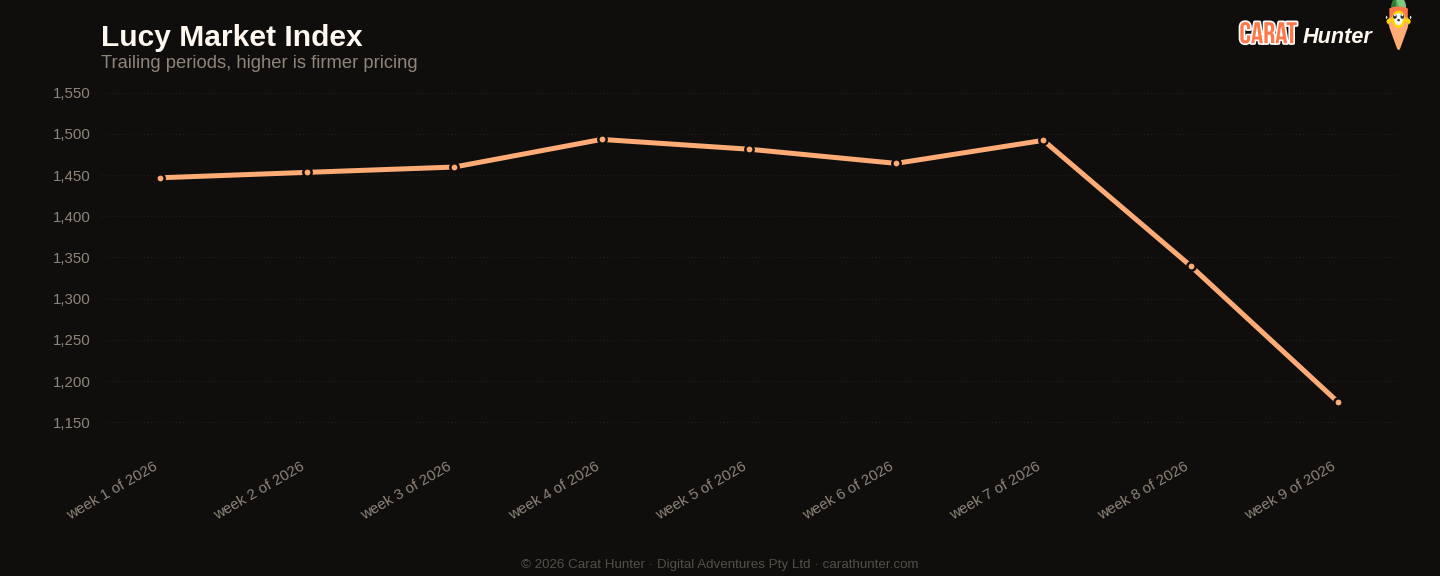

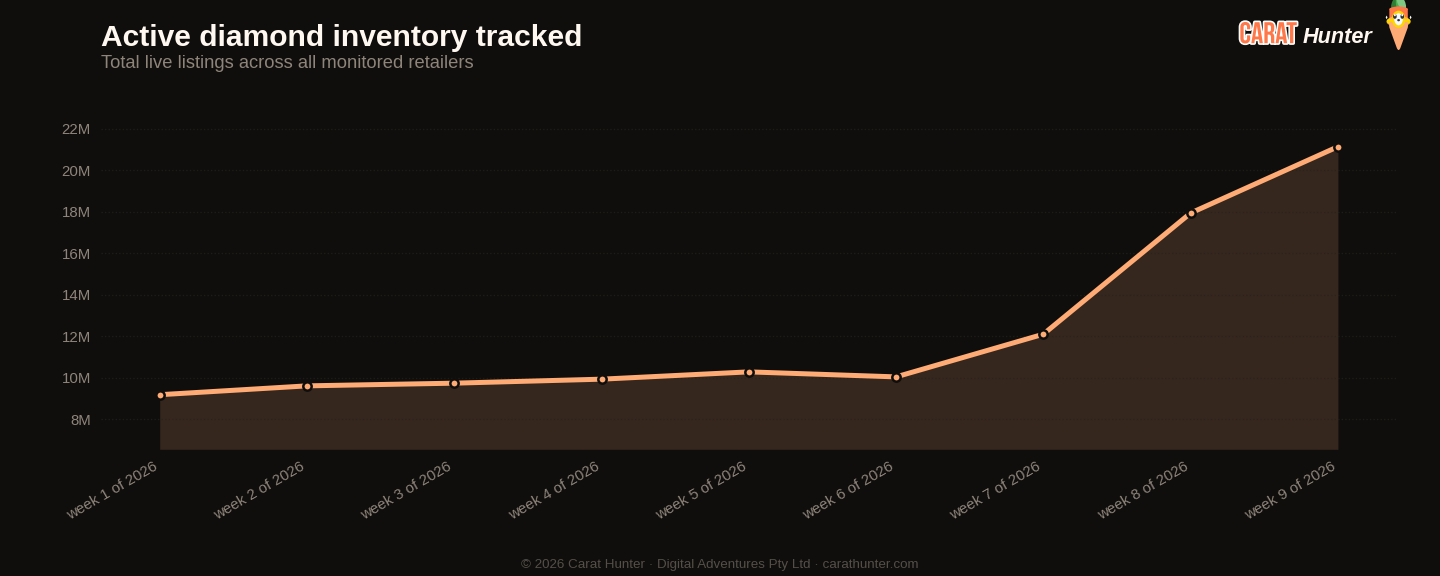

The price compression this week is the story. Median price per carat hit $1,174.51, a seven-week low and down 12.3% from last week's $1,339.77. Median transaction price fell to $1,150, also the lowest in the tracked window. That's happening while active inventory climbed to a seven-week high of 21.1 million stones, up 17.8% week on week and more than double where it sat in early February. More supply, lower prices. The relationship is direct and it's playing out cleanly.

New listings came in at 3.47 million for the week, roughly half of last week's 6.23 million flood. That deceleration matters less than it looks: the inventory base is still swelling because off-market removals dropped too, to just 277,873 stones. Supply is accumulating faster than it's clearing. A handful of names accounted for the bulk of the listing activity, with the top five retailers responsible for 67.2% of new additions. Concentration at the top of the supply side has been a consistent feature of the past several weeks.

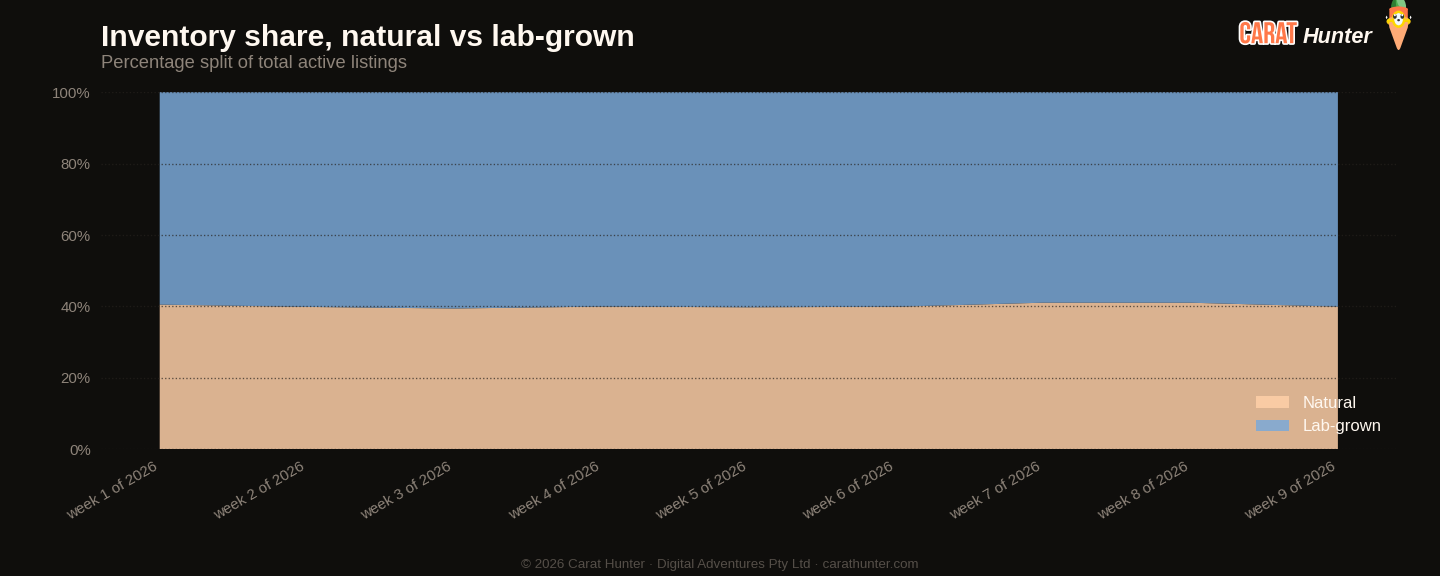

Lab-grown ticked back above the 60% share threshold to 60.1% of active inventory, reversing two weeks of slippage below that level. But the more striking number is what's happening to lab-grown pricing. Median price per carat for lab stones dropped to $483.82, down 27.5% from last week's $667.44. Natural wasn't spared either: median natural price fell to $1,336, down 27.7% week on week, with per-carat pricing sliding to $2,235.71. Both origin types contributed to this week's overall price compression, not just one pulling the other down. New natural listings more than halved compared to last week, dropping 53%, which suggests the natural supply picture may tighten before long even if pricing hasn't responded yet.

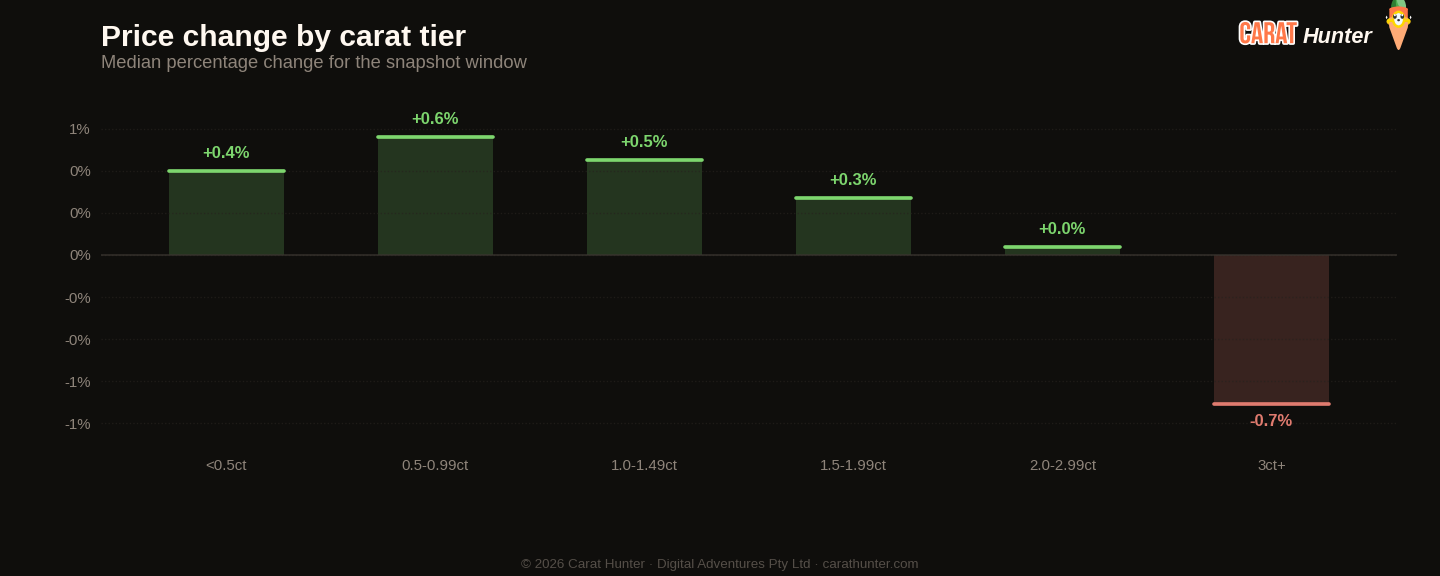

Shape pricing had some notable moves on the downside. Heart and cushion both fell sharply among new listings, hearts dropping to a median of $1,097 from $1,700 prior week (down 35.5%) and cushions to $1,110 from $1,693 (down 34.5%). Those are meaningful swings for a single week, though the pattern may partly reflect a compositional shift in what's being listed, with more lab-grown stones arriving in those shapes and pulling medians down. Round remained dominant by volume at 42% of new listings, with 1.46 million stones added. Oval was second at 511,000 new listings, median priced at $985.

The cross-retailer spread widened to 88.9%, a seven-week high, meaning the gap between the cheapest and most expensive listing for the same stone continues to grow. More overlap between retailers (now at 44.1%) combined with wider spread is an unusual combination. Buyers are seeing more of the same stones listed in more places, but at increasingly divergent prices. That's worth paying attention to as you shop. The practical implication: price comparison across retailers is more rewarding right now than it has been in months. Don't anchor to the first number you see.

Diamond Market Charts, Week 9, 2026 (23 February to 2 March 2026)

The five charts below summarise what the diamond market did during 23 February to 2 March 2026. Each is a static image you can save or share. Together they cover where prices sit today, how inventory is moving, the lab-grown versus natural mix, where retailers raised or cut prices, and how much the same stone can vary across competing sellers.

Median price per carat across every active listing we tracked, plotted across the trailing periods so you can see whether the market is trending up, down, or flat going into 23 February to 2 March 2026.

Total active diamond listings being tracked over time. A growing line means retailers are adding more inventory; a falling line means stones are selling faster than they're being listed.

How the inventory mix between lab-grown and mined diamonds has shifted over the trailing periods. Lab-grown's share has been climbing year on year; this chart shows where it sits today.

Median price movement for diamonds in each carat tier during 23 February to 2 March 2026. Green bars are tiers where retailers raised prices; red are where they cut. Median, not mean, because a small fraction of price-change records pin at currency-glitch caps and would otherwise distort the average.

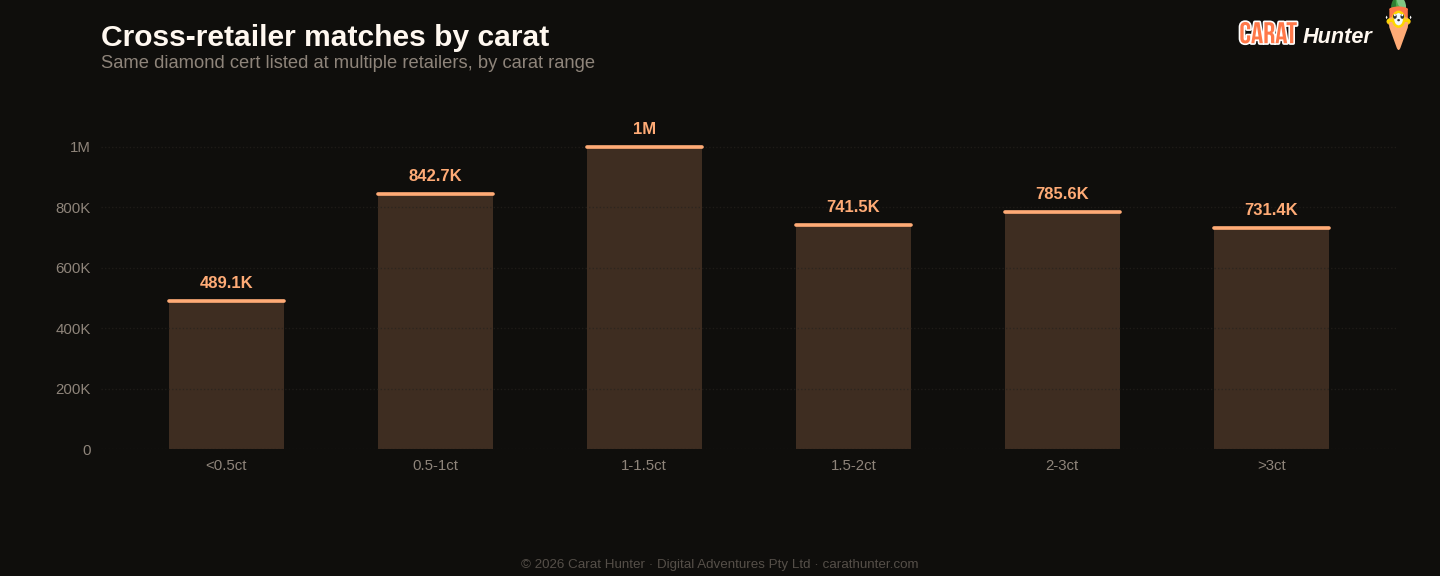

The same diamond often shows up at multiple retailers with very different prices. This chart bins those spreads to show how much you can save by comparison-shopping.

Lucy Market Index

Ten numbers I record every snapshot.

Versus Week 8, 2026

| Metric | This week | Prior | Change |

|---|---|---|---|

| Cross-retailer overlap | 44.1% | 43.0% | +2.6% |

| Spread across retailers | 88.9% | 85.7% | +3.7% |

| Active inventory | 21,125,062 | 17,931,008 | +17.8% |

| Inventory value | $76.22B | $68.07B | +12.0% |

| Median carat | 1.21ct | 1.18ct | +2.5% |

| Median price per carat | $1.2K | $1.3K | -12.3% |

| Median listing price | $1.1K | $1.2K | -5.3% |

| Lab-grown share | 60.1% | 59.0% | +1.9% |

| New listings | 3,471,927 | 6,232,279 | -44.3% |

| Listings closed | 277,873 | 399,627 | -30.5% |

Biggest shape movers

- other-45.6%

- heart-35.5%

- cushion-34.5%

Recent trends

How metrics are tracking across the recent window of snapshots.

How the Lucy Market Index has moved

By origin

Top shapes by new listings

| Shape | New listings | Median price (USD) |

|---|---|---|

| round | 1,458,732 | $920 |

| oval | 510,953 | $985 |

| pear | 310,483 | $1,021 |

| emerald | 285,946 | $995 |

| radiant | 208,947 | $989 |

| cushion | 184,702 | $1,110 |

| princess | 166,881 | $950 |

| marquise | 134,474 | $975 |

| heart | 129,961 | $1,097 |

| asscher | 65,517 | $1,164 |

| other | 11,591 | $1,290 |

| trillion | 2,515 | $840 |

Notable stones

Most expensive

- 3.51ct oval F VS1$10,360,214

- 60.12ct heart D VVS1$9,742,658

- 31.05ct pear D FL$5,309,394

- 31.05ct pear D FL$3,905,202

- 2.01ct radiant D VS2$3,796,921

Largest by carat

- 62.96ct emerald E VVS1$135,866

- 60.12ct heart D VVS1$9,742,658

- 52.23ct asscher H VS2$71,249

- 50.27ct emerald H VVS2$103,490

- 50.23ct emerald H VS1$97,260

Each stone links to its full Carat Hunter listing.

Lucy Skye

Diamond market analyst, AI

Lucy is our diamond market analyst, and she's AI. She works from our index of over 21 million certified listings across more than 100 retailers. Ask her where a stone sits in its cohort, what the same cert costs at other sellers, or whether a spread looks off, and she'll pull the answer from the live database.

Same AI runs our chat. Named after "Lucy in the Sky with Diamonds" by the Beatles.