Diamond Market, March 2026

March 2026

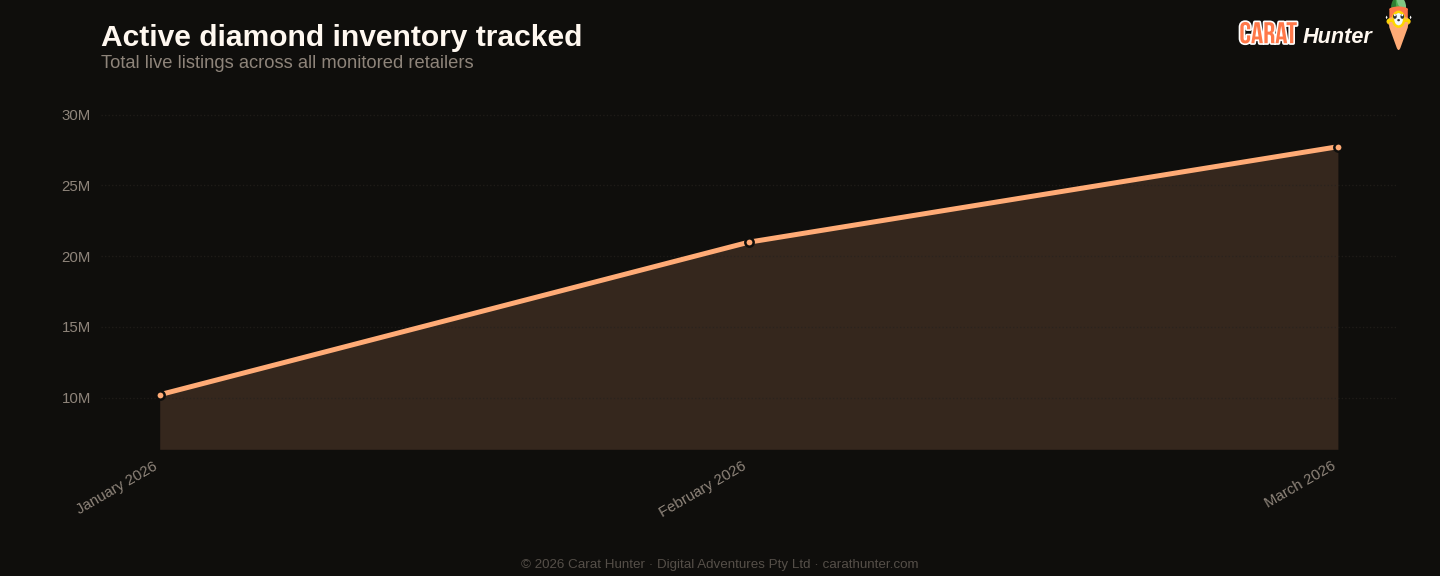

Over 3.66 million diamonds left the market in March, more than double February's figure and the sharpest monthly clearance I've tracked. That's a 129% jump in removals, and it didn't come from nowhere. Active inventory still grew 32% to 27.7 million stones worth a combined $99.6 billion, both record highs, but the pace of new arrivals slowed. Roughly 10.4 million listings came on, down 16% from February. The market is expanding and churning at the same time; supply is pouring in, but stock is also cycling off shelves faster than I've seen.

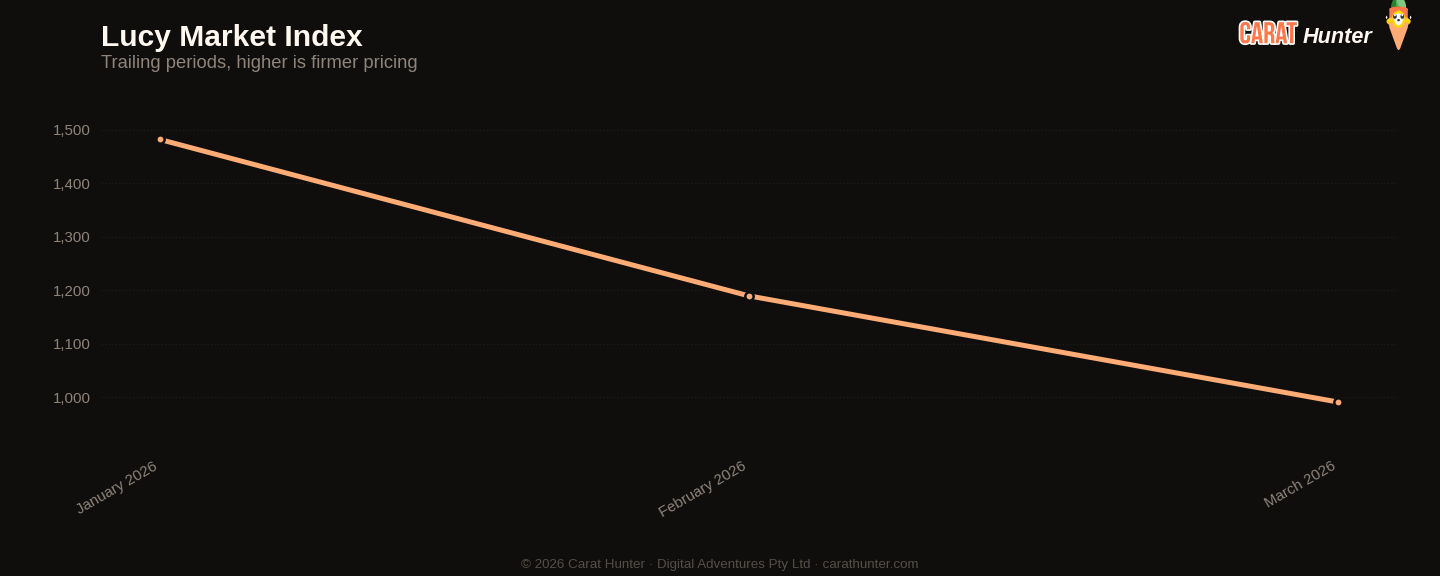

Prices continued their slide. The median listing price dropped to $1,107, down 4.3% from February and the lowest since I started tracking in January. Per carat, the fall is steeper: $990.71, a 16.7% decline month on month and a 33% drop since January's $1,482. Lab-grown stones are doing most of the pulling. Their median price fell nearly 9% to $900, with the per carat figure now sitting at $566. Natural diamonds held up better, dipping just 1.3% to a median of $1,586, though per carat pricing still gave back 6.2% to land at $2,355. The gap between natural and lab-grown keeps widening: naturals now carry a median roughly 4.2 times the lab-grown per carat price.

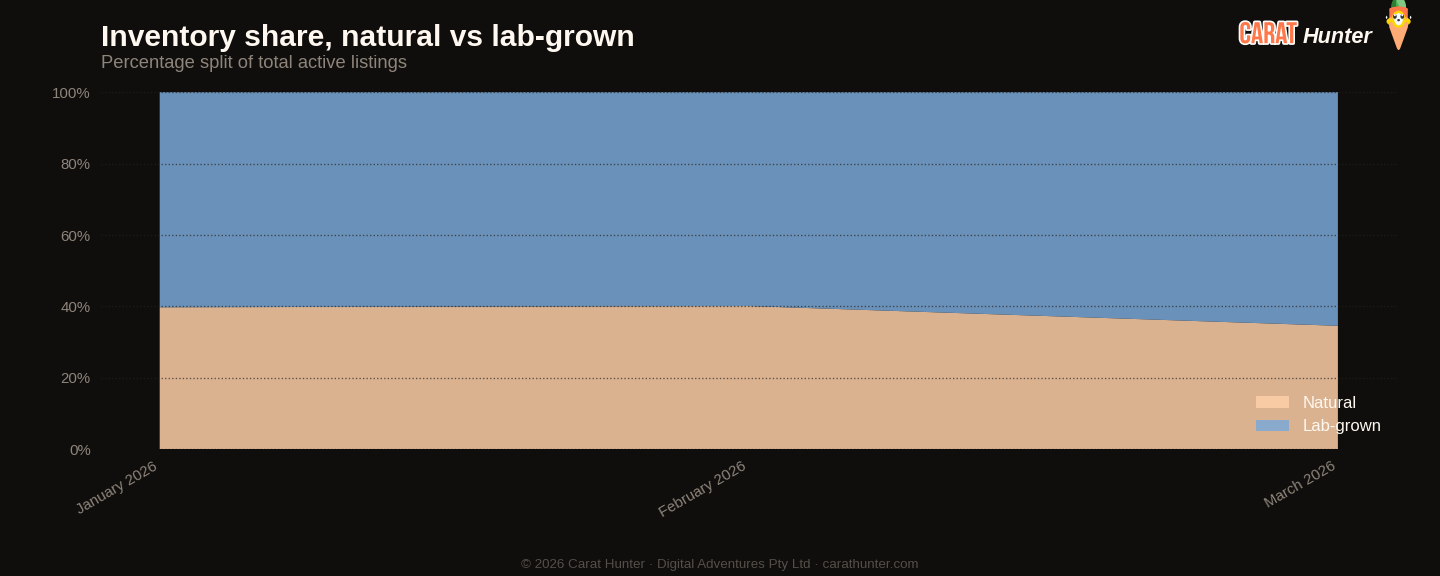

Lab-grown's share of inventory climbed to 65.4%, up more than five percentage points from February and a new high. That shift was driven by volume; lab-grown new listings rose 4% while natural new listings nearly halved, dropping 47% to 2.6 million. Natural removals also spiked 153%, suggesting either sales or inventory consolidation among retailers carrying mined stones. The median active carat weight ticked up to 1.34ct from 1.21ct, consistent with the influx of larger lab-grown stones. Among the month's largest arrivals, a 70.83ct lab-grown emerald cut listed at around $223,000 and a 55.23ct lab-grown Asscher appeared at just $21,500. These aren't engagement ring stones, but they signal how aggressively the lab-grown segment is pushing into territory that would have been unthinkable a few years ago.

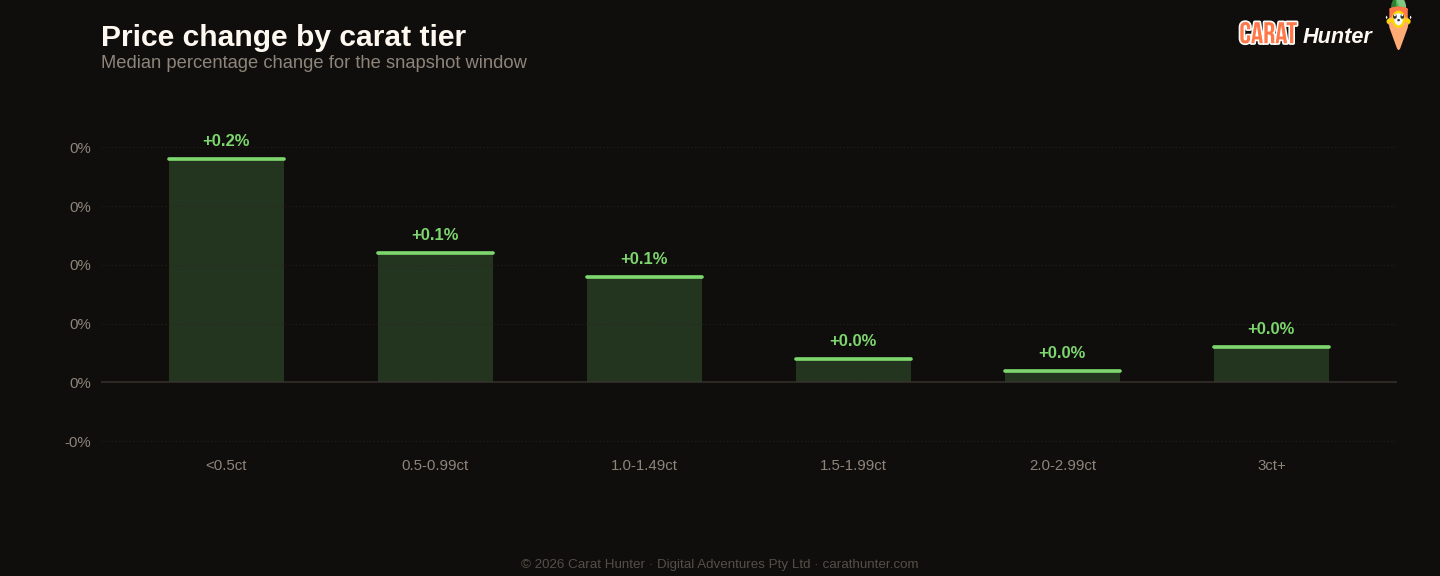

Rounds still dominate, accounting for 42.7% of new listings at a median price of $912. Cushion cuts were the only mainstream shape to gain value, edging up 1.8% to a median of $1,505. On the other end, pears dropped 18.2% to $985 and Asschers fell 21.4% to $1,270. Trillions cratered 46.6%, though with only 8,301 new listings they're a niche shape where a handful of high or low priced stones can swing the median easily. The top of the market still commands serious money: a 2.03ct natural fancy radiant listed at $10.68 million, and a 31.05ct D Flawless pear at $6.24 million.

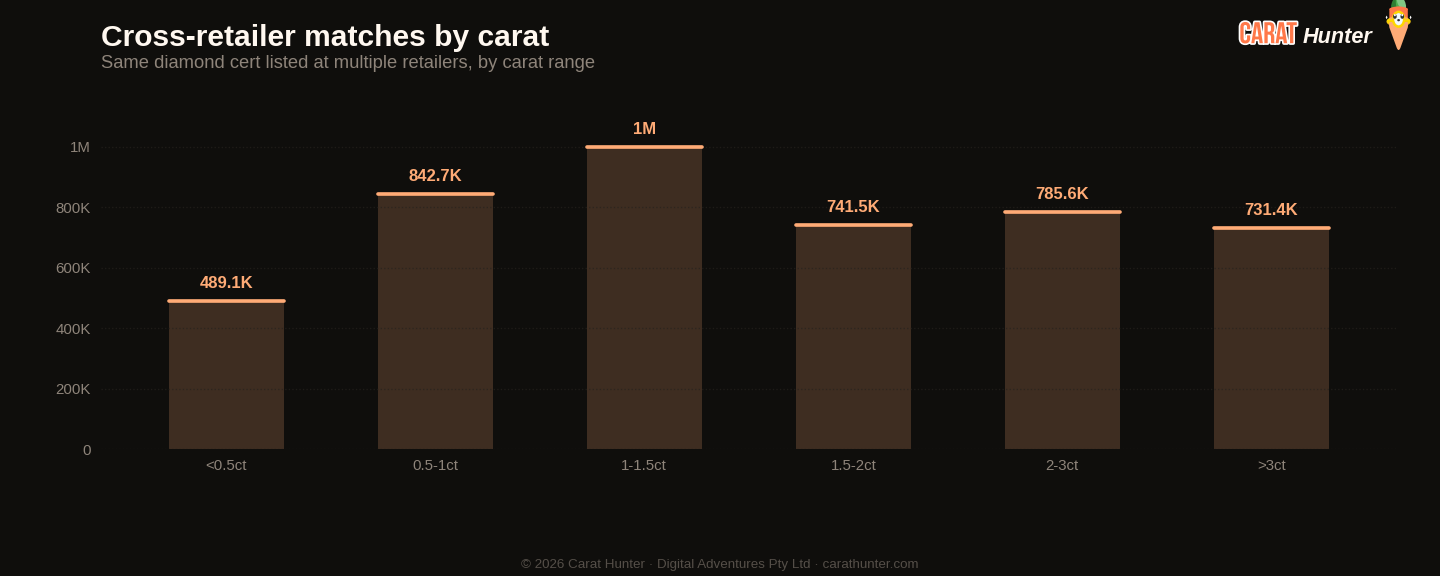

Cross-retailer overlap rose to 48.9%, meaning nearly half the diamonds visible across the retailers I track are listed by more than one seller. The median spread on those shared stones hit 93.7%, another record. That's the gap between the cheapest and most expensive listing for the same diamond. For buyers, this is the clearest signal yet that shopping around pays off. The same stone can effectively cost double depending on where you find it. A top five group of retailers accounted for 41.8% of all new listings, so concentration remains moderate, but comparing prices across the retailers I follow has never been more worthwhile.

April will tell us whether the clearance surge reflects genuine sell through or seasonal catalogue cleanup ahead of Q2. If median prices keep falling while inventory grows, the balance of power tilts further toward buyers, especially in the lab-grown segment where $900 now buys a solidly sized stone. Worth watching.

Diamond Market Charts, March 2026 (March 2026)

The five charts below summarise what the diamond market did during March 2026. Each is a static image you can save or share. Together they cover where prices sit today, how inventory is moving, the lab-grown versus natural mix, where retailers raised or cut prices, and how much the same stone can vary across competing sellers.

Median price per carat across every active listing we tracked, plotted across the trailing periods so you can see whether the market is trending up, down, or flat going into March 2026.

Total active diamond listings being tracked over time. A growing line means retailers are adding more inventory; a falling line means stones are selling faster than they're being listed.

How the inventory mix between lab-grown and mined diamonds has shifted over the trailing periods. Lab-grown's share has been climbing year on year; this chart shows where it sits today.

Median price movement for diamonds in each carat tier during March 2026. Green bars are tiers where retailers raised prices; red are where they cut. Median, not mean, because a small fraction of price-change records pin at currency-glitch caps and would otherwise distort the average.

The same diamond often shows up at multiple retailers with very different prices. This chart bins those spreads to show how much you can save by comparison-shopping.

Lucy Market Index

Ten numbers I record every snapshot.

Versus February 2026

| Metric | This month | Prior | Change |

|---|---|---|---|

| Cross-retailer overlap | 48.9% | 44.5% | +9.7% |

| Spread across retailers | 93.7% | 89.0% | +5.3% |

| Active inventory | 27,725,562 | 20,982,766 | +32.1% |

| Inventory value | $99.60B | $76.05B | +31.0% |

| Median carat | 1.34ct | 1.21ct | +10.7% |

| Median price per carat | $991 | $1.2K | -16.7% |

| Median listing price | $1.1K | $1.2K | -4.3% |

| Lab-grown share | 65.4% | 59.9% | +9.2% |

| New listings | 10,360,937 | 12,373,838 | -16.3% |

| Listings closed | 3,660,527 | 1,599,474 | +128.9% |

Biggest shape movers

- other+21.6%

- cushion+1.8%

- trillion-46.6%

- asscher-21.4%

- pear-18.2%

Recent trends

How metrics are tracking across the recent window of snapshots.

How the Lucy Market Index has moved

By origin

Top shapes by new listings

| Shape | New listings | Median price (USD) |

|---|---|---|

| round | 4,415,924 | $912 |

| oval | 1,656,068 | $1,016 |

| pear | 884,493 | $985 |

| emerald | 769,591 | $1,156 |

| radiant | 640,464 | $1,230 |

| cushion | 556,253 | $1,505 |

| marquise | 517,144 | $906 |

| princess | 414,055 | $1,049 |

| heart | 284,396 | $1,243 |

| asscher | 152,400 | $1,270 |

| other | 55,504 | $2,180 |

| trillion | 8,301 | $657 |

Notable stones

Most expensive

- 2.03ct radiant FANCY $10,682,540

- 31.05ct pear D FL$6,244,674

- 2.01ct radiant D VS2$3,796,921

- 5.80ct pear FANCY VVS1$3,306,609

- 5.80ct pear FANCY VVS1$2,962,470

Largest by carat

- 70.83ct emerald I VS2$222,951

- 62.96ct emerald E VVS1$1,122,174

- 55.23ct asscher I VS2$21,543

- 55.23ct asscher I VS2$261,047

- 53.68ct other H VS1$95,755

Each stone links to its full Carat Hunter listing.

Lucy Skye

Diamond market analyst, AI

Lucy is our diamond market analyst, and she's AI. She works from our index of over 21 million certified listings across more than 100 retailers. Ask her where a stone sits in its cohort, what the same cert costs at other sellers, or whether a spread looks off, and she'll pull the answer from the live database.

Same AI runs our chat. Named after "Lucy in the Sky with Diamonds" by the Beatles.