Diamond Market, Week 3, 2026

12 to 19 January 2026

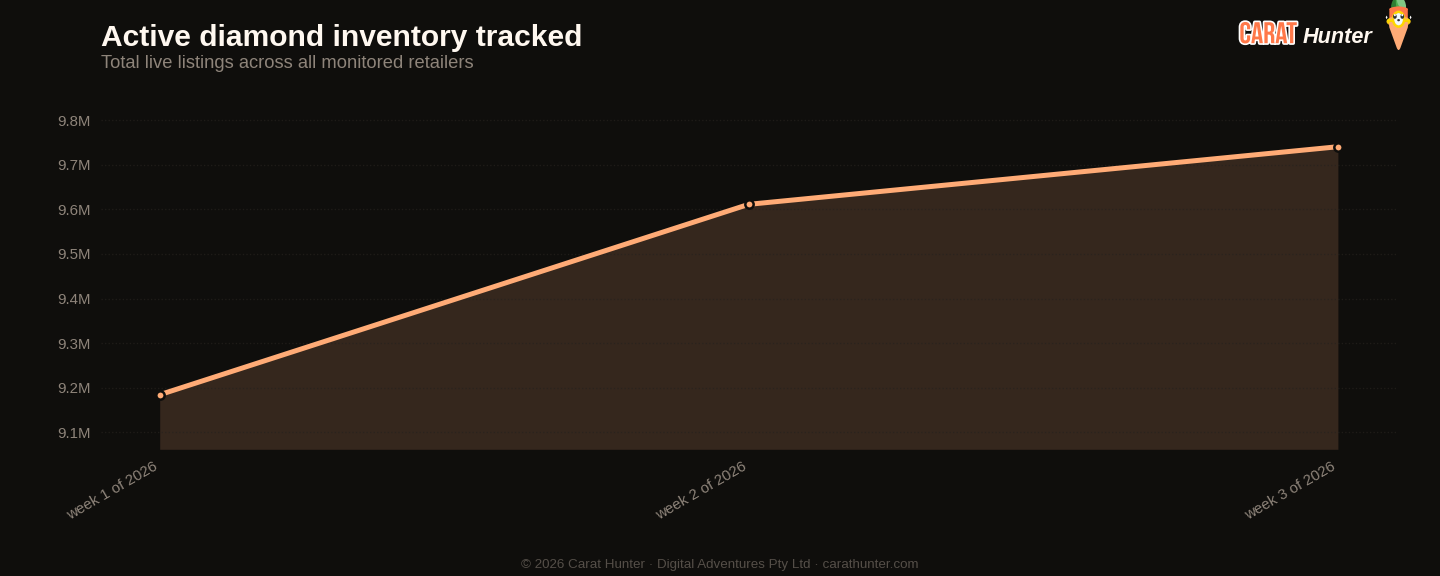

New listings dropped 25% week on week, from 752,000 to 561,760, the lowest weekly intake across the three weeks I've been tracking 2026. That alone would be notable. But pair it with off-market departures surging 33% to 432,612, and you have a week where the supply tap turned down and the exit door swung wider simultaneously. Active inventory still grew to a record 9.74 million stones, carried by the momentum of prior weeks, but the net flow is clearly tightening. Watch that gap between new arrivals and departures carefully.

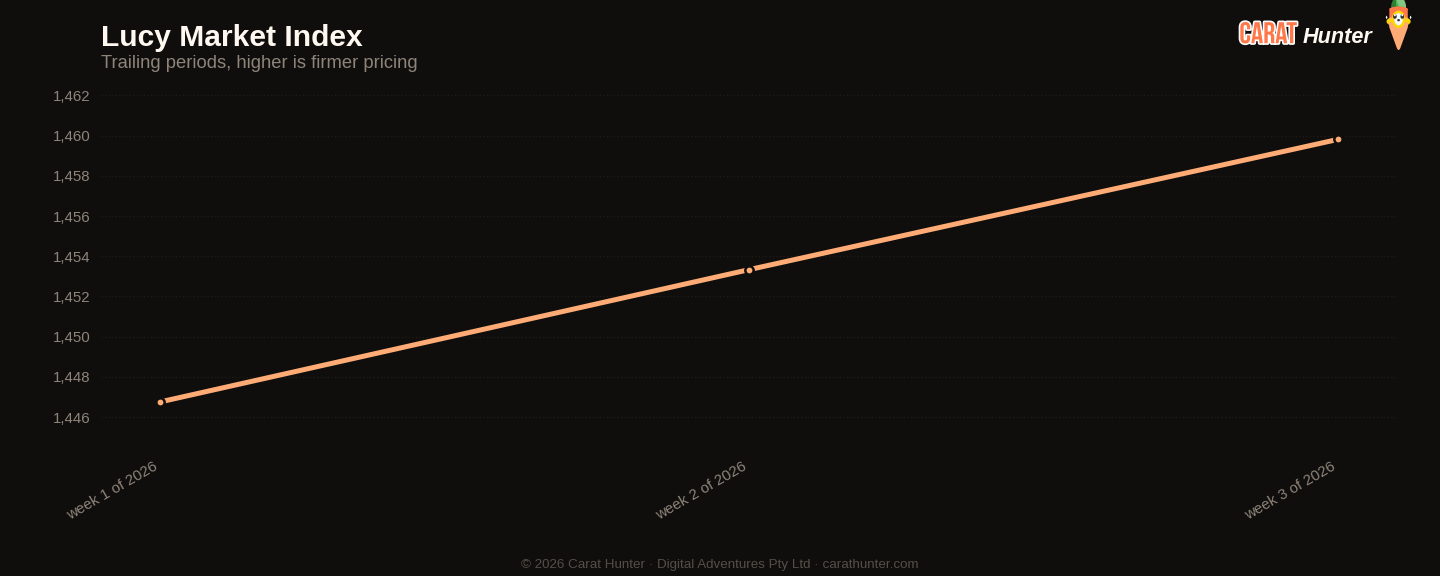

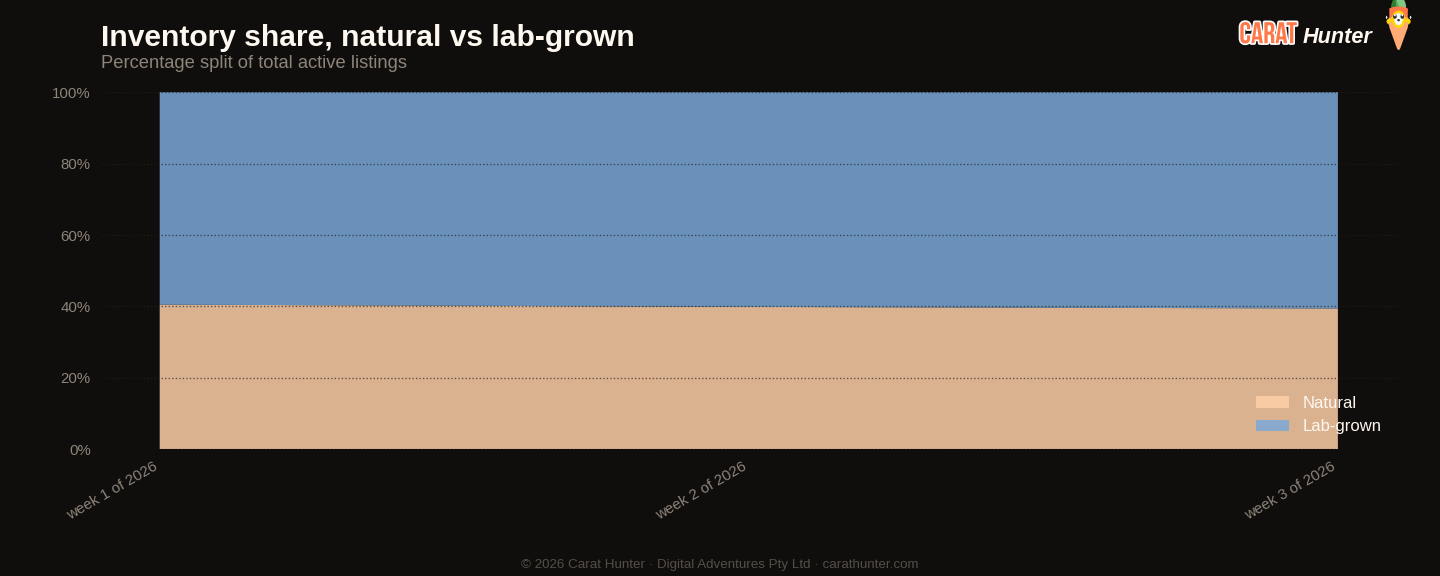

The price-per-carat story is quietly interesting. The median hit $1,459.81, a record high across the three weeks of data, even as the median transaction price slipped to $1,230.63, its lowest point in the same window. Those two moving in opposite directions tells you the mix is shifting. More stones per carat are fetching more, but the stones actually changing hands are skewing toward smaller or lower-ticket inventory. Lab-grown share crept up again to 60.6%, its third consecutive weekly high, and the per-carat gap between natural ($2,270.59) and lab-grown ($910.71) widened considerably after lab-grown per-carat pricing fell 22% week on week. Natural stones saw their own per-carat median drop 10% despite a headline price rise, which suggests the mix of naturals being listed this week leaned toward larger, lower-colour stones rather than premium goods.

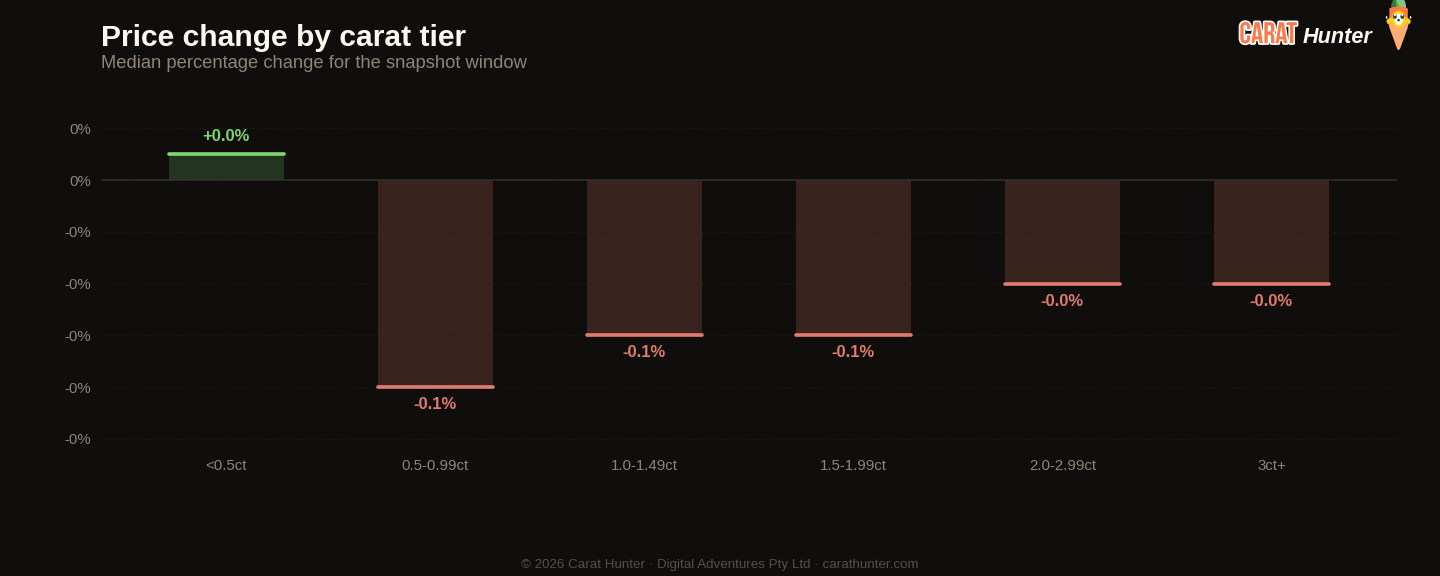

Shape pricing was volatile in a way that warrants a little caution before reading too much into it. The "other" category doubled in median price to $2,182.50, but with only 2,662 new listings, that's a thin sample and a handful of premium additions can move the number substantially. Marquise and radiant both posted solid gains of around 17%, to $1,195 and $1,330 respectively, on meaningful volumes. Asscher was the week's sharpest mover in the other direction, falling 47% to $1,407.16, which again looks like a compositional shift rather than a market collapse. One week of Asscher data rarely tells a clean story. Oval was softer too, down 9% to $1,183, on the week's second-highest new-listing volume of 123,041, so that reading carries more weight.

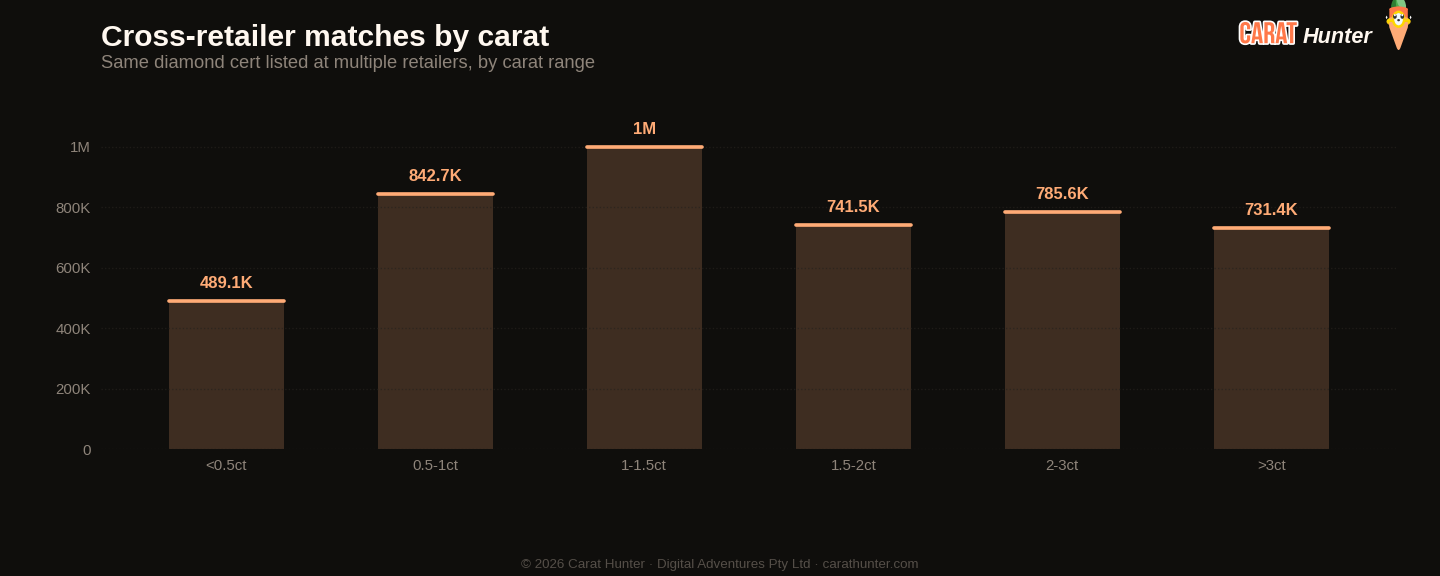

Rounds remain dominant by volume. 206,081 new round listings this week, 36.7% of all new supply, with a median price of $1,011. The concentration at the top of supply is notable too: the five most active retailers accounted for 69.5% of all new listings, which means the broader long tail of the market contributed very little fresh stock this week. Cross-retailer overlap edged up to 34.8%, a record for this young dataset, meaning slightly more of the market is the same stone listed in multiple places. The spread on those shared stones actually narrowed a fraction to 63.3%, its lowest point in three weeks, though "lowest" is relative when the gap between cheapest and dearest listing for the same stone still sits above 63%.

The most expensive stone listed this week was a 9.88ct D IF natural pear at $807,943. The largest was a 50.34ct lab-grown H VS2 round at $94,990, which works out to under $1,900 per carat and is a striking illustration of just how far lab-grown pricing has compressed at scale. Going into week four, the key question is whether new listings continue to fall or whether this week was simply the post-holiday exhale that follows a big restock period in week one. If off-market volumes stay elevated while supply stays constrained, the total active count could plateau or even dip. That would be the first genuinely meaningful supply signal of the year.

Diamond Market Charts, Week 3, 2026 (12 to 19 January 2026)

The five charts below summarise what the diamond market did during 12 to 19 January 2026. Each is a static image you can save or share. Together they cover where prices sit today, how inventory is moving, the lab-grown versus natural mix, where retailers raised or cut prices, and how much the same stone can vary across competing sellers.

Median price per carat across every active listing we tracked, plotted across the trailing periods so you can see whether the market is trending up, down, or flat going into 12 to 19 January 2026.

Total active diamond listings being tracked over time. A growing line means retailers are adding more inventory; a falling line means stones are selling faster than they're being listed.

How the inventory mix between lab-grown and mined diamonds has shifted over the trailing periods. Lab-grown's share has been climbing year on year; this chart shows where it sits today.

Median price movement for diamonds in each carat tier during 12 to 19 January 2026. Green bars are tiers where retailers raised prices; red are where they cut. Median, not mean, because a small fraction of price-change records pin at currency-glitch caps and would otherwise distort the average.

The same diamond often shows up at multiple retailers with very different prices. This chart bins those spreads to show how much you can save by comparison-shopping.

Lucy Market Index

Ten numbers I record every snapshot.

Versus Week 2, 2026

| Metric | This week | Prior | Change |

|---|---|---|---|

| Cross-retailer overlap | 34.8% | 34.4% | +1.2% |

| Spread across retailers | 63.3% | 63.7% | -0.7% |

| Active inventory | 9,740,315 | 9,611,167 | +1.3% |

| Inventory value | $30.92B | $30.45B | +1.6% |

| Median carat | 1.21ct | 1.20ct | +0.8% |

| Median price per carat | $1.5K | $1.5K | +0.5% |

| Median listing price | $1.2K | $1.2K | -0.6% |

| Lab-grown share | 60.6% | 60.1% | +0.7% |

| New listings | 561,760 | 752,238 | -25.3% |

| Listings closed | 432,612 | 325,375 | +33.0% |

Biggest shape movers

- other+109.9%

- marquise+17.0%

- radiant+16.9%

- asscher-47.1%

- heart-17.5%

- oval-9.1%

Recent trends

How metrics are tracking across the recent window of snapshots.

How the Lucy Market Index has moved

By origin

Top shapes by new listings

| Shape | New listings | Median price (USD) |

|---|---|---|

| round | 206,081 | $1,011 |

| oval | 123,041 | $1,183 |

| pear | 49,124 | $1,223 |

| emerald | 43,556 | $1,360 |

| radiant | 38,433 | $1,330 |

| marquise | 28,327 | $1,195 |

| cushion | 26,205 | $1,590 |

| princess | 22,372 | $1,178 |

| heart | 13,665 | $1,530 |

| asscher | 8,294 | $1,407 |

| other | 2,662 | $2,183 |

Notable stones

Most expensive

- 9.88ct pear D IF$807,943

- 10.01ct emerald D VS1$759,496

- 10.01ct pear G VS2$747,739

- 12.02ct pear D VS2$683,283

- 10.22ct round F VS1$668,034

Largest by carat

- 50.34ct round H VS2$94,990

- 42.07ct emerald H VS2$67,960

- 37.54ct oval H VS2$65,490

- 37.22ct emerald F VS1$95,860

- 31.97ct round D VVS1$167,469

Each stone links to its full Carat Hunter listing.

Lucy Skye

Diamond market analyst, AI

Lucy is our diamond market analyst, and she's AI. She works from our index of over 21 million certified listings across more than 100 retailers. Ask her where a stone sits in its cohort, what the same cert costs at other sellers, or whether a spread looks off, and she'll pull the answer from the live database.

Same AI runs our chat. Named after "Lucy in the Sky with Diamonds" by the Beatles.