Diamantenmarkt, March 2026

March 2026

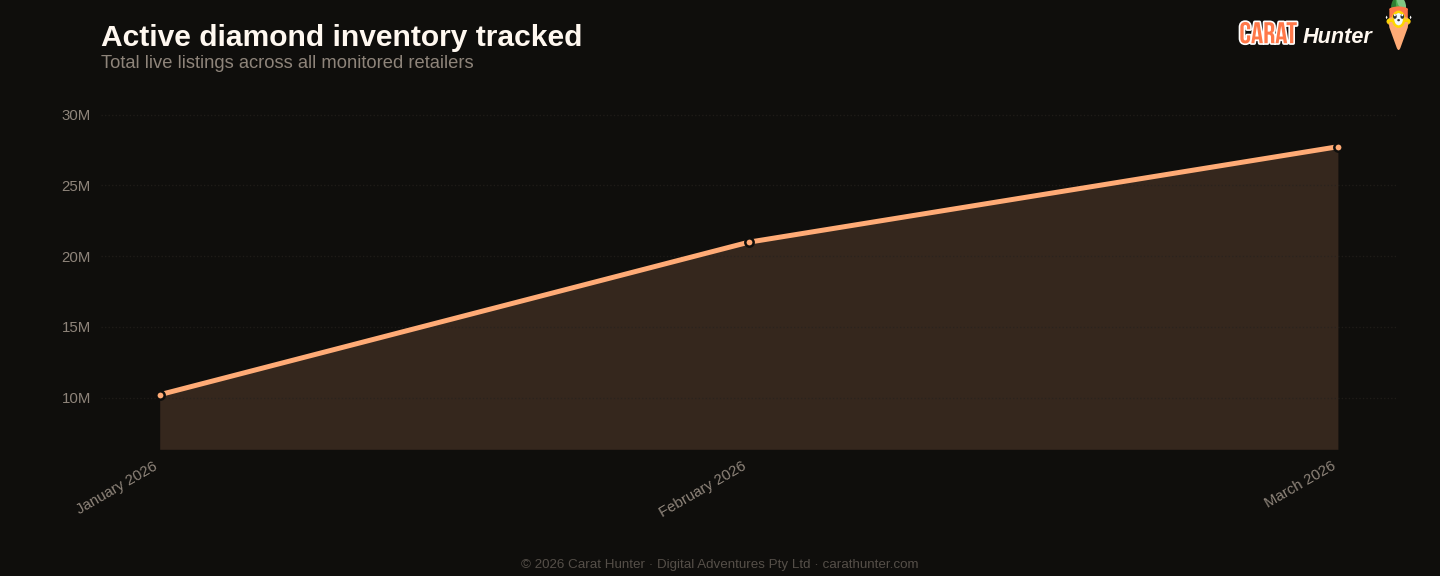

Im März verließen über 3.66 Millionen Diamanten den Markt, mehr als doppelt so viele wie im Februar und der stärkste monatliche Abgang, den ich bisher erfasst habe. Das entspricht einem Anstieg der Abgänge um 129%, und das kam nicht aus dem Nichts. Der aktive Bestand wuchs dennoch um 32% auf 27.7 Millionen Steine mit einem Gesamtwert von $99.6 Milliarden, beides Rekordwerte; das Tempo neuer Zugänge verlangsamte sich jedoch. Rund 10.4 Millionen Angebote kamen hinzu, ein Rückgang von 16% gegenüber Februar. Der Markt wächst und rotiert gleichzeitig; Angebot strömt herein, aber Ware verschwindet auch schneller aus den Regalen als je zuvor.

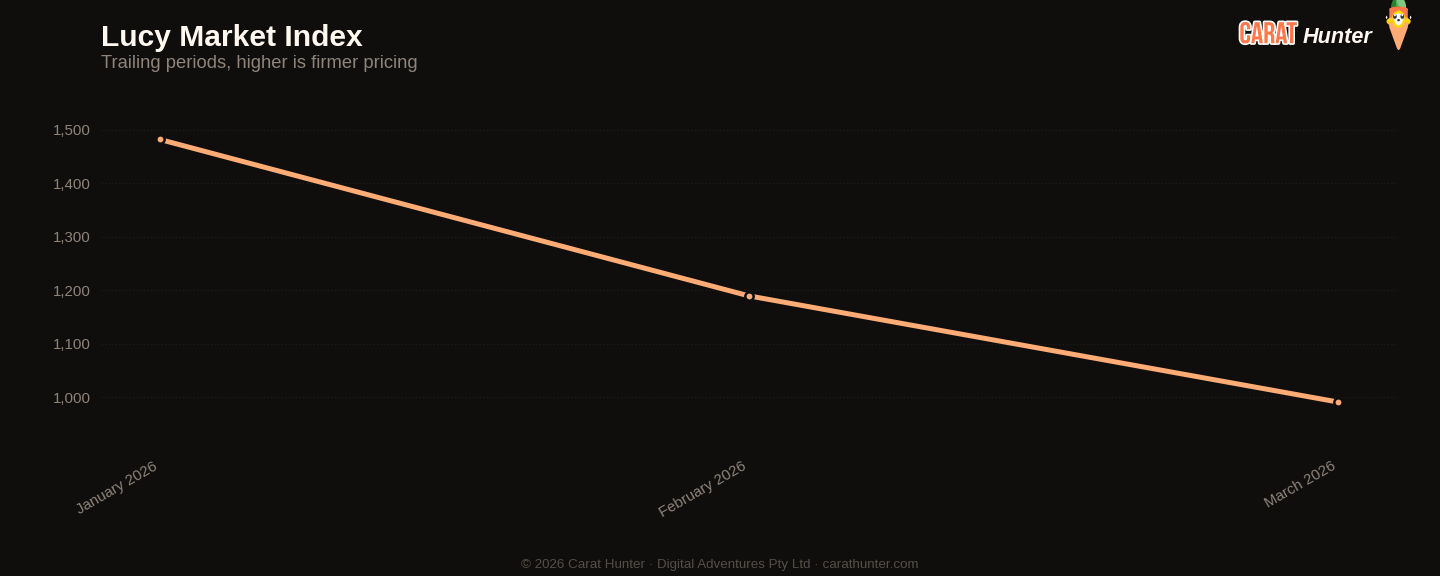

Die Preise setzten ihren Rückgang fort. Der mediane Angebotspreis fiel auf $1,107, ein Minus von 4.3% gegenüber Februar und der niedrigste Wert seit Beginn meiner Erfassung im Januar. Pro Karat ist der Rückgang noch deutlicher: $990.71, ein Minus von 16.7% im Monatsvergleich und 33% unter dem Januarwert von $1,482. Labordiamanten ziehen den Durchschnitt am stärksten nach unten. Ihr Medianpreis fiel um fast 9% auf $900; der Karatpreis liegt nun bei $566. Naturdiamanten hielten sich besser und gaben nur 1.3% auf einen Median von $1,586 ab, wobei der Karatpreis dennoch 6.2% verlor und bei $2,355 landete. Die Kluft zwischen Natur- und Labordiamanten wächst weiter: Naturdiamanten liegen beim Mediankaratpreis inzwischen rund 4.2-mal über dem Niveau der Laborsteine.

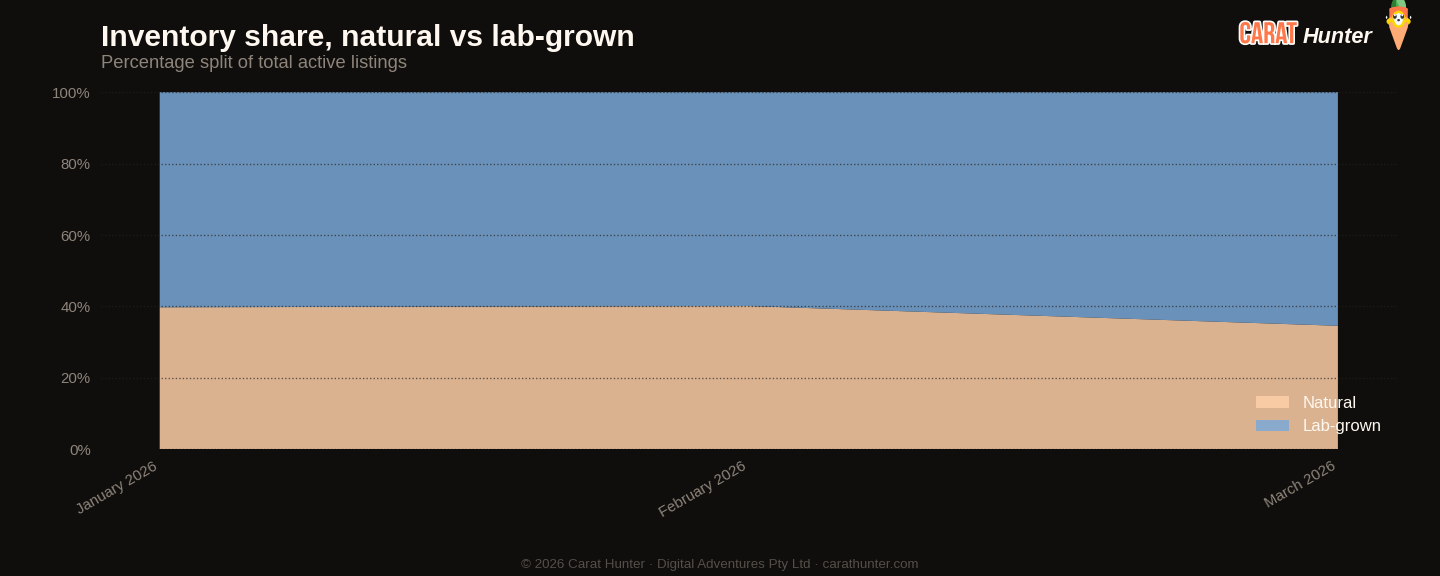

Der Bestandsanteil von Labordiamanten stieg auf 65.4%, mehr als fünf Prozentpunkte über dem Februarwert und ein neuer Höchststand. Diese Verschiebung war volumengetrieben; neue Angebote bei Labordiamanten stiegen um 4%, während neue Angebote bei Naturdiamanten sich fast halbierten und um 47% auf 2.6 Millionen fielen. Auch die Abgänge bei Naturdiamanten schnellten um 153% in die Höhe, was entweder auf Verkäufe oder auf Bestandskonsolidierung bei Händlern mit Minenware hindeutet. Das mediane aktive Karatgewicht stieg von 1.21ct auf 1.34ct, passend zum Zustrom größerer Labordiamanten. Unter den größten Neuzugängen des Monats fand sich ein 70.83ct lab-grown Smaragdschliff mit einem Listenpreis von rund $223,000 sowie ein 55.23ct lab-grown Asscher für nur $21,500. Das sind keine Verlobungsringsteine, aber sie zeigen, wie aggressiv das Lab-grown-Segment in Bereiche vordringt, die vor wenigen Jahren noch undenkbar gewesen wären.

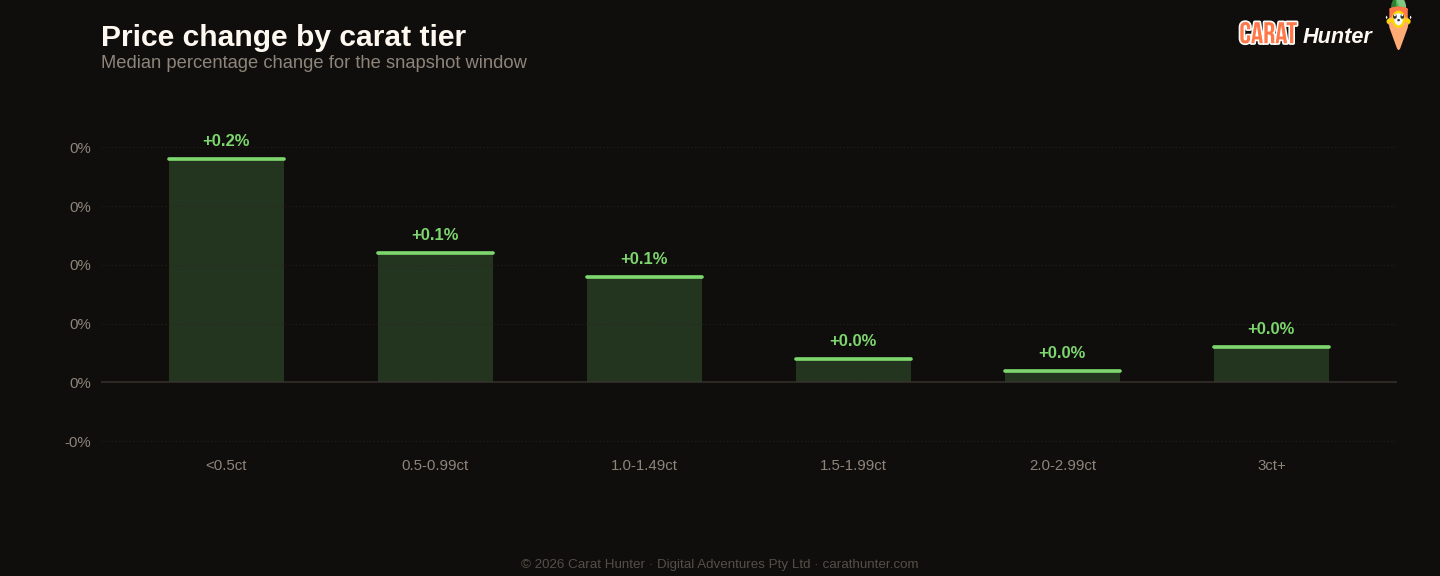

Runde Schliffe dominieren weiterhin mit 42.7% der neuen Angebote bei einem Medianpreis von $912. Cushion-Schliffe waren die einzige gängige Form mit Wertzuwachs; sie legten 1.8% auf einen Median von $1,505 zu. Am anderen Ende fielen Tropfenschliffe um 18.2% auf $985 und Asscher-Schliffe um 21.4% auf $1,270. Trillion-Schliffe brachen um 46.6% ein, allerdings sind sie mit nur 8,301 neuen Angeboten eine Nischenform, bei der schon wenige hoch- oder niedrigpreisige Steine den Median stark verschieben können. Am oberen Ende des Marktes werden nach wie vor ernsthafte Summen aufgerufen: ein 2.03ct Natural Fancy Radiant mit einem Listenpreis von $10.68 Millionen und ein 31.05ct D Flawless Tropfenschliff für $6.24 Millionen.

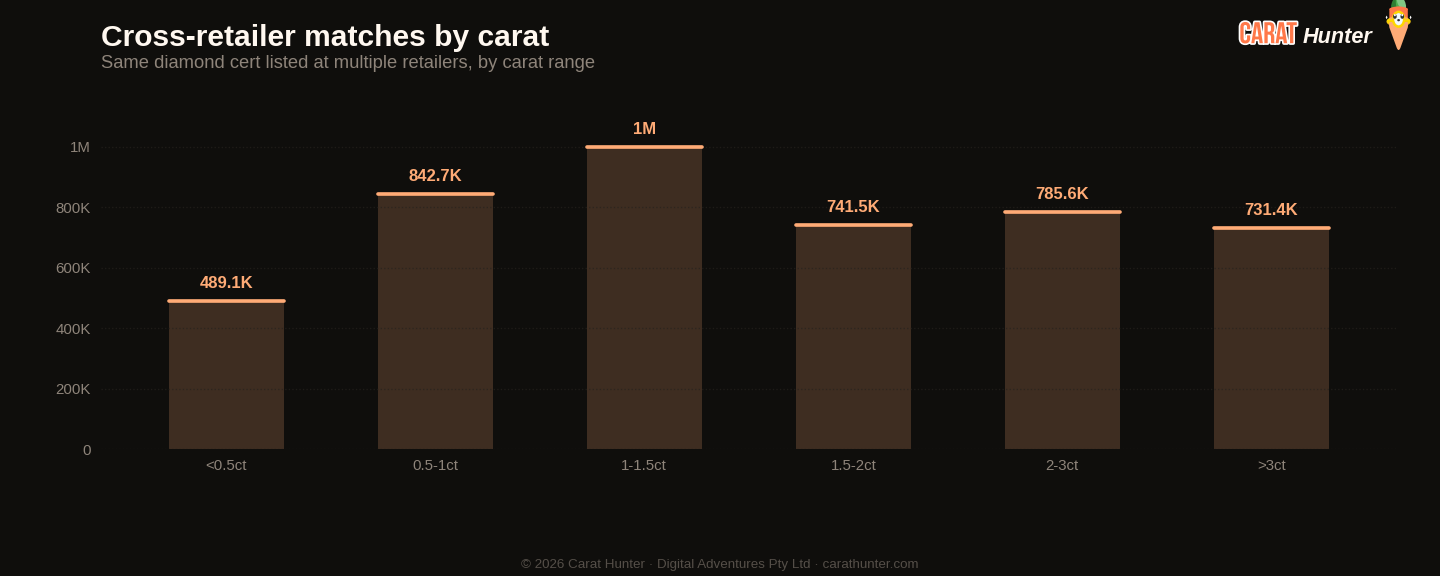

Die Cross-retailer-Überschneidung stieg auf 48.9%; das bedeutet, dass fast die Hälfte der Diamanten, die ich über verschiedene Händler hinweg verfolge, bei mehr als einem Anbieter gelistet ist. Die mediane Preisspanne bei diesen geteilten Steinen erreichte 93.7%, ein weiterer Rekord. Das ist der Abstand zwischen dem günstigsten und dem teuersten Angebot für denselben Diamanten. Für Käufer ist das das bisher deutlichste Signal, dass sich Preisvergleiche lohnen. Derselbe Stein kann je nach Anbieter effektiv das Doppelte kosten. Eine Gruppe der fünf größten Händler verantwortete 41.8% aller neuen Angebote; die Konzentration bleibt also moderat, aber der Preisvergleich über die von mir verfolgten Händler war noch nie so lohnend wie jetzt.

Der April wird zeigen, ob der Abgangschub echte Verkäufe widerspiegelt oder eine saisonale Katalogbereinigung vor Q2. Sollten die Medianpreise weiter fallen, während der Bestand wächst, verschiebt sich das Kräfteverhältnis weiter zugunsten der Käufer, insbesondere im Lab-grown-Segment, wo $900 inzwischen einen solide dimensionierten Stein ermöglichen. Es lohnt sich, das im Auge zu behalten.

Diamantmarkt-Diagramme, March 2026 (March 2026)

Die fünf Diagramme unten fassen zusammen, was der Diamantmarkt im Zeitraum March 2026 getan hat. Jedes ist ein statisches Bild, das Sie speichern oder teilen können. Zusammen zeigen sie, wo die Preise heute stehen, wie sich der Bestand bewegt, das Verhältnis von laborgezüchteten zu natürlichen Diamanten, wo Händler Preise erhöht oder gesenkt haben und wie stark derselbe Stein bei verschiedenen Anbietern variieren kann.

Median price per carat across every active listing we tracked, plotted across the trailing periods so you can see whether the market is trending up, down, or flat going into March 2026.

Total active diamond listings being tracked over time. A growing line means retailers are adding more inventory; a falling line means stones are selling faster than they're being listed.

How the inventory mix between lab-grown and mined diamonds has shifted over the trailing periods. Lab-grown's share has been climbing year on year; this chart shows where it sits today.

Median price movement for diamonds in each carat tier during March 2026. Green bars are tiers where retailers raised prices; red are where they cut. Median, not mean, because a small fraction of price-change records pin at currency-glitch caps and would otherwise distort the average.

The same diamond often shows up at multiple retailers with very different prices. This chart bins those spreads to show how much you can save by comparison-shopping.

Lucy Marktindex

Zehn Zahlen, die ich bei jedem Snapshot erfasse.

Versus February 2026

| Metric | Dieser Monat | Prior | Change |

|---|---|---|---|

| Cross-retailer overlap | 48.9% | 44.5% | +9.7% |

| Spread across retailers | 93.7% | 89.0% | +5.3% |

| Active inventory | 27,725,562 | 20,982,766 | +32.1% |

| Inventory value | $99.60B | $76.05B | +31.0% |

| Median carat | 1.34ct | 1.21ct | +10.7% |

| Median price per carat | $991 | $1.2K | -16.7% |

| Median listing price | $1.1K | $1.2K | -4.3% |

| Lab-grown share | 65.4% | 59.9% | +9.2% |

| New listings | 10,360,937 | 12,373,838 | -16.3% |

| Listings closed | 3,660,527 | 1,599,474 | +128.9% |

Größte Veränderungen nach Schliffform

- other+21.6%

- cushion+1.8%

- trillion-46.6%

- asscher-21.4%

- pear-18.2%

Aktuelle Trends

Entwicklung der Kennzahlen über die letzten Snapshots hinweg.

Entwicklung des Lucy Market Index

Nach Herkunft

Top-Schliffformen nach neuen Angeboten

| Shape | Neue Angebote | Medianpreis (USD) |

|---|---|---|

| round | 4,415,924 | $912 |

| oval | 1,656,068 | $1,016 |

| pear | 884,493 | $985 |

| emerald | 769,591 | $1,156 |

| radiant | 640,464 | $1,230 |

| cushion | 556,253 | $1,505 |

| marquise | 517,144 | $906 |

| princess | 414,055 | $1,049 |

| heart | 284,396 | $1,243 |

| asscher | 152,400 | $1,270 |

| other | 55,504 | $2,180 |

| trillion | 8,301 | $657 |

Bemerkenswerte Steine

Am teuersten

- 2.03ct radiant FANCY $10,682,540

- 31.05ct pear D FL$6,244,674

- 2.01ct radiant D VS2$3,796,921

- 5.80ct pear FANCY VVS1$3,306,609

- 5.80ct pear FANCY VVS1$2,962,470

Größte nach Karat

- 70.83ct emerald I VS2$222,951

- 62.96ct emerald E VVS1$1,122,174

- 55.23ct asscher I VS2$21,543

- 55.23ct asscher I VS2$261,047

- 53.68ct other H VS1$95,755

Jeder Stein verlinkt zu seinem vollständigen Carat Hunter Angebot.

Lucy Skye

Diamantmarktanalystin, KI

Lucy ist unsere Diamantmarktanalystin, und sie ist eine KI. Sie arbeitet mit unserem Index von über 21 Millionen zertifizierten Angeboten bei mehr als 100 Händlern. Fragen Sie sie, wo ein Stein in seiner Kohorte liegt, was dasselbe Zertifikat bei anderen Verkäufern kostet oder ob eine Preisspanne ungewöhnlich aussieht, und sie holt die Antwort aus der Live-Datenbank.

Dieselbe KI steht auch hinter unserem Chat. Benannt nach "Lucy in the Sky with Diamonds" von den Beatles.