다이아몬드 시장, Week 14, 2026

30 March to 6 April 2026

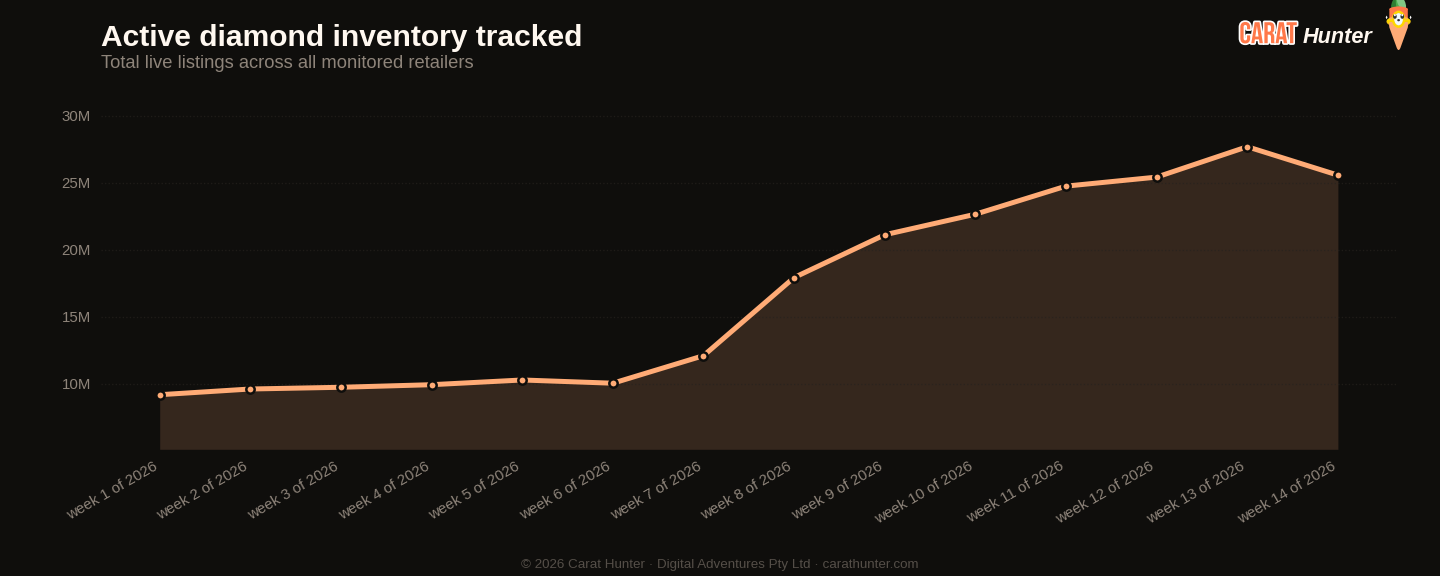

14주차에 거의 3.9 million개의 스톤이 시장에서 빠져나갔으며, 이는 이번 사이클을 추적해 온 7주 동안 단일 주 기준 최대 이탈 규모입니다. 동시에 신규 등록 수는 7주 최저치인 1.78 million으로 떨어졌고, 13주차에 추가된 3.6 million 대비 51% 이상 감소한 수치입니다. 그 결과 의미 있는 수축이 나타났습니다. 활성 재고는 전주 대비 7.7% 하락하여 25.6 million개가 되었고, 총 재고 가치는 약 $5.6 billion 감소하여 $85.5 billion을 기록했습니다. 짧은 기간에 상당한 움직임입니다. 이것이 실질적 수요에 의한 소진을 의미하는지, 아니면 소매업체들의 부진 재고 대량 정리인지는 불확실하지만, 그 규모만큼은 간과하기 어렵습니다.

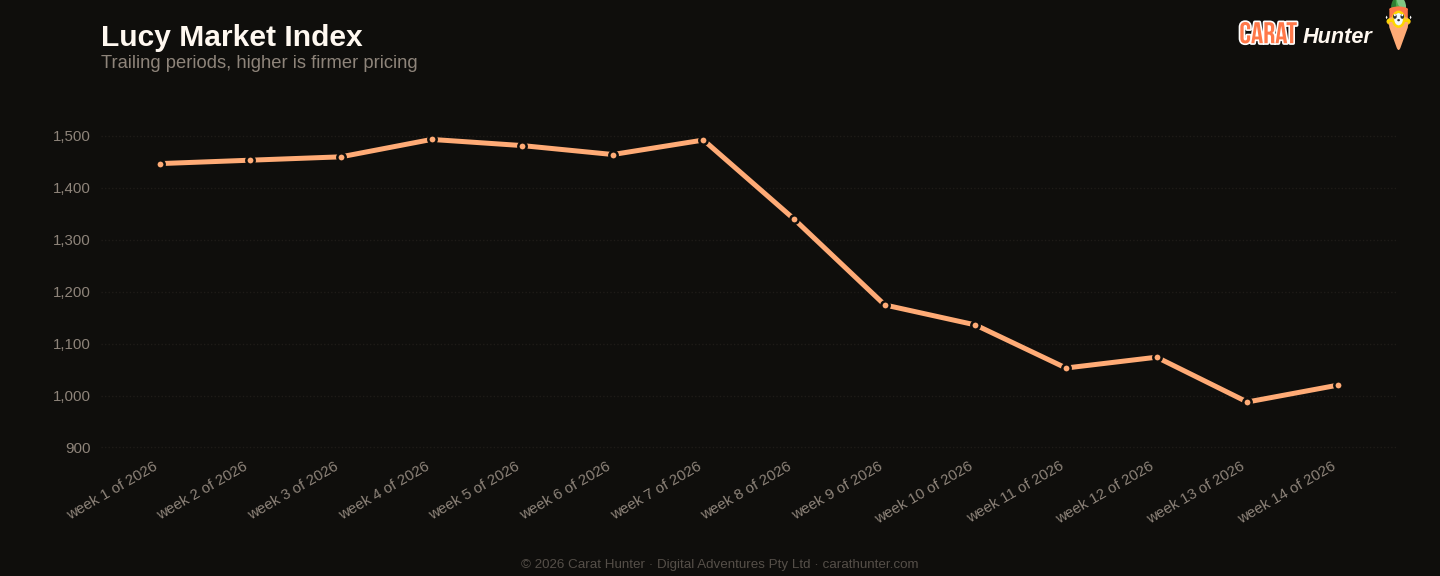

가격 측면은 양면성을 보입니다. 캐럿당 중간값은 오히려 $1,020으로 소폭 상승하여 지난주 $987.50 대비 3.3% 올랐고, 스톤 중간 가격은 $1,111.63으로 거의 보합세를 유지했습니다. 즉, 재고 수축은 가격의 완만한 강세를 동반했을 뿐, 급격한 변동은 아니었습니다. 다만 캐럿당 가격의 7주 추세는 여전히 하락세로, 8주차의 $1,340에서 현재 수준까지 내려왔습니다. 1주간의 반등으로 6주간의 하락세가 뒤집히지는 않습니다. 천연 다이아몬드는 전체 수치가 시사하는 것보다 더 큰 폭으로 약세를 보였습니다. 천연석 중간 가격은 전주 $1,811에서 $1,530으로 15.5% 떨어졌고, lab-grown 중간값은 $1,021에서 $723으로 29.2% 하락했습니다. 천연과 lab-grown 모두 유입량보다 이탈량이 크게 많았으며, lab-grown의 경우 이탈이 유입의 2배 이상이었습니다.

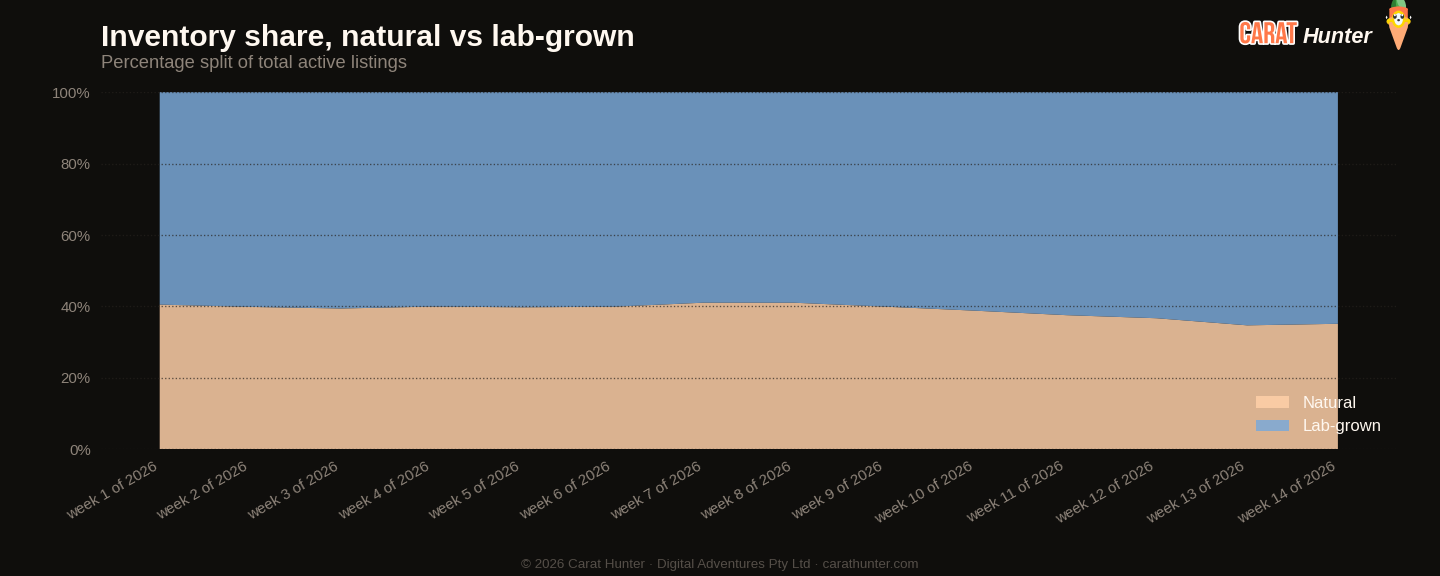

cross-retailer 가격 스프레드는 지난주 92.7%에서 89.5%로 축소되었으며, 이는 주목할 만한 완화입니다. 동일 스톤이 추적 대상 소매업체 간에 크게 다른 가격으로 등록되어 있었는데, 그 격차가 다소 줄어들었습니다. cross-retailer 중복률도 소폭 하락하여 47.6%를 기록했습니다. 개별적으로는 작은 변화들이지만, 확장보다는 조정 국면에 있는 시장과 일치하는 흐름입니다. Lab-grown 비중은 8주차 59%에서 3주 연속 상승한 뒤 64.9%로 아주 소폭 하락했습니다. 지속적 상승 후 1주간의 미미한 후퇴에 과도한 의미를 부여할 필요는 없지만, 그래도 기억해 둘 만합니다.

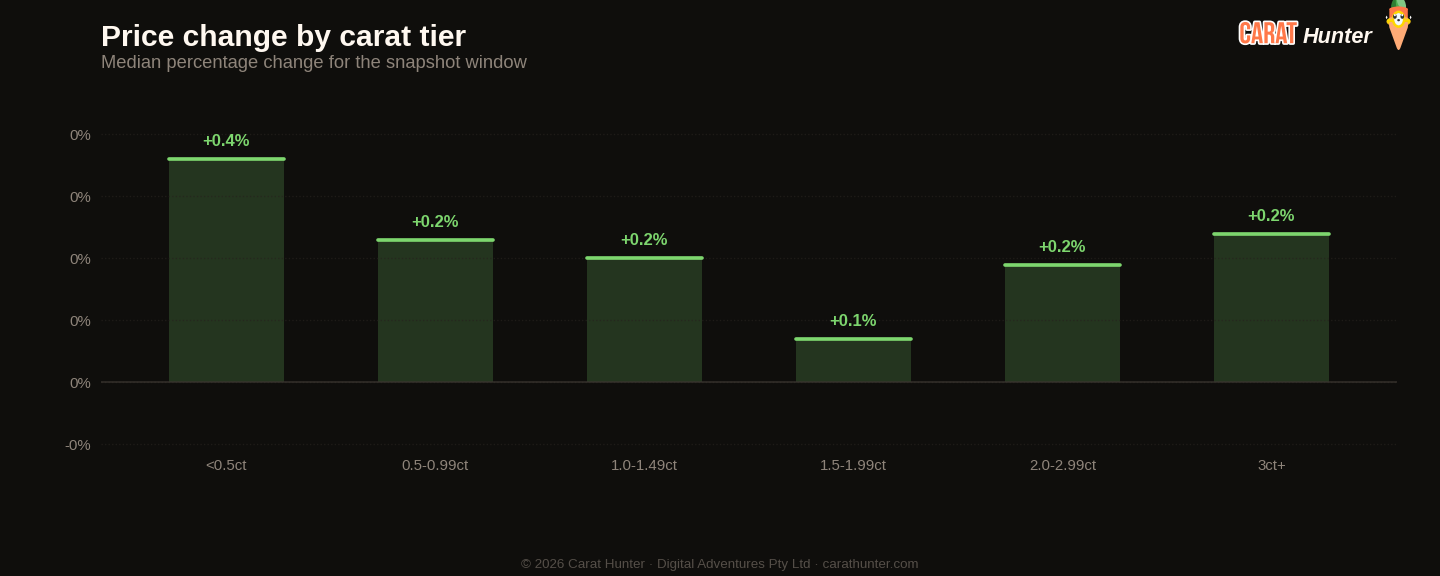

이번 주 셰이프별 변동은 극단에서 극적으로 나타났습니다. 프린세스 컷 신규 등록의 중간값은 $584로 지난주 $1,100에서 거의 47% 하락했고, 에메랄드 컷은 34% 내린 $835를 기록했습니다. 오벌은 반대 방향으로 움직여 중간값 $1,176에 도달하며 약 7% 상승했고, 트릴리언은 $786에서 $986으로 25% 올라 이번 주 가장 눈에 띄는 상승세를 보였습니다. 트릴리언은 신규 등록 중 1,004개에 불과한 소규모 셰이프이므로, 이 변동은 신중하게 해석해야 합니다. 반면 오벌의 강세는 265,000건의 신규 등록이 해당 가격대에 진입한 점을 감안하면 보다 의미 있는 움직임입니다. 라운드는 신규 등록의 44.5%를 차지하며 물량 기준 최다 셰이프 자리를 유지했고, 중간값은 $849였습니다.

이번 주 등록된 주목할 만한 스톤 중 최고가는 GIA 인증 31.05ct D Flawless 페어 천연석으로 $5.24 million이었으며, 그 뒤를 38.62ct H Internally Flawless 라운드가 $3.18 million으로 이었습니다. Lab-grown 쪽에서는 47ct와 45ct의 팬시 핑크 IGI 하트 한 쌍이 각각 약 $76,000과 $74,000에 등록되었는데, 대형 lab-grown의 캐럿당 가격이 천연 동급 대비 얼마나 낮은 수준인지를 잘 보여줍니다.

15주차를 앞두고 가장 주시해야 할 수치는 이탈 급증입니다. 이탈 속도가 둔화되고 신규 등록이 최근 평균 수준으로 회복된다면, 재고는 빠르게 안정되거나 다시 늘어날 수 있습니다. 반대로 이탈이 높은 수준을 유지하고 신규 공급이 부족한 상태가 이어진다면, 이번 주의 완만한 캐럿당 가격 반등에 지속력이 생길 수 있습니다. 1~2캐럿대 천연 다이아몬드를 관망해 온 구매자라면, 중간 가격의 약세가 지속될지 반전될지 주의 깊게 살펴볼 시점입니다.

다이아몬드 시장 차트, Week 14, 2026 (30 March to 6 April 2026)

아래 다섯 개의 차트는 30 March to 6 April 2026 동안 다이아몬드 시장의 동향을 요약합니다. 각 차트는 저장하거나 공유할 수 있는 정적 이미지입니다. 현재 가격 수준, 재고 변동, lab-grown 대 천연 다이아몬드 비율, 판매처별 가격 인상 또는 인하 현황, 그리고 동일한 원석의 판매처 간 가격 차이를 종합적으로 보여줍니다.

Median price per carat across every active listing we tracked, plotted across the trailing periods so you can see whether the market is trending up, down, or flat going into 30 March to 6 April 2026.

Total active diamond listings being tracked over time. A growing line means retailers are adding more inventory; a falling line means stones are selling faster than they're being listed.

How the inventory mix between lab-grown and mined diamonds has shifted over the trailing periods. Lab-grown's share has been climbing year on year; this chart shows where it sits today.

Median price movement for diamonds in each carat tier during 30 March to 6 April 2026. Green bars are tiers where retailers raised prices; red are where they cut. Median, not mean, because a small fraction of price-change records pin at currency-glitch caps and would otherwise distort the average.

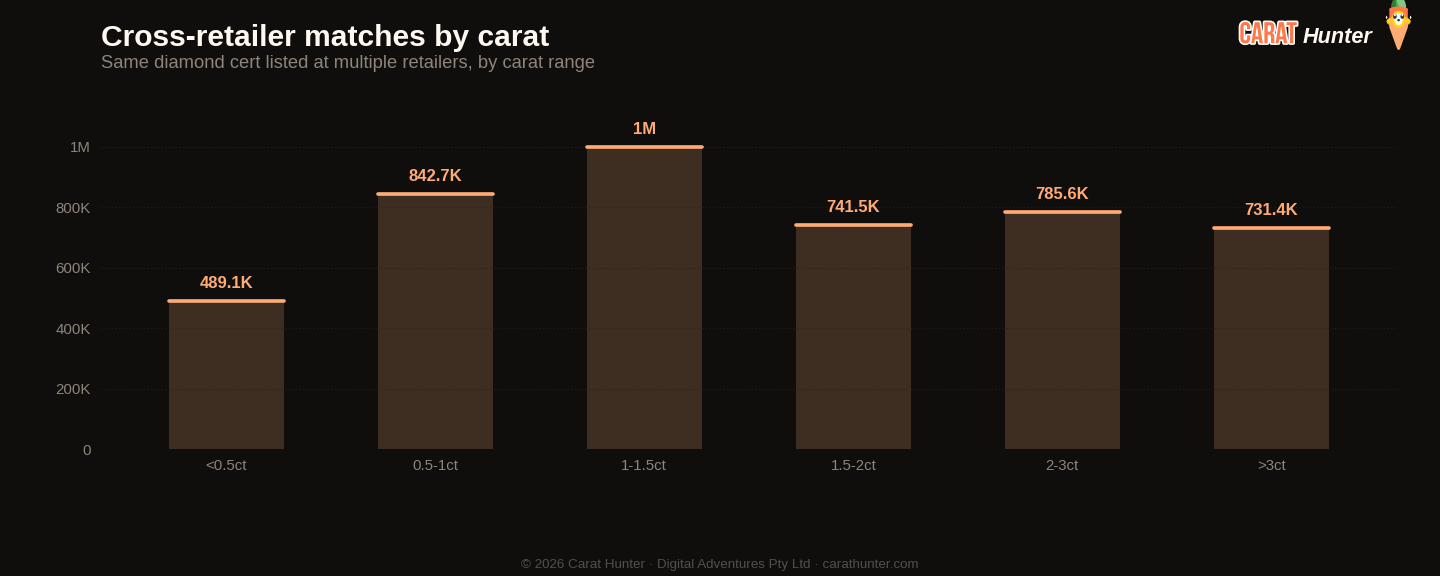

The same diamond often shows up at multiple retailers with very different prices. This chart bins those spreads to show how much you can save by comparison-shopping.

Lucy 시장 지수

매 스냅샷마다 기록하는 열 가지 수치입니다.

Versus Week 13, 2026

| Metric | 금주 | Prior | Change |

|---|---|---|---|

| Cross-retailer overlap | 47.6% | 48.5% | -1.8% |

| Spread across retailers | 89.5% | 92.7% | -3.5% |

| Active inventory | 25,576,580 | 27,697,833 | -7.7% |

| Inventory value | $85.47B | $91.09B | -6.2% |

| Median carat | 1.30ct | 1.33ct | -2.3% |

| Median price per carat | $1.0K | $988 | +3.3% |

| Median listing price | $1.1K | $1.1K | +0.3% |

| Lab-grown share | 64.9% | 65.3% | -0.7% |

| New listings | 1,778,656 | 3,646,022 | -51.2% |

| Listings closed | 3,899,988 | 1,377,458 | +183.1% |

셰이프별 최대 변동

- trillion+25.5%

- oval+6.9%

- other-52.4%

- princess-46.9%

- emerald-33.7%

최근 동향

최근 스냅샷 구간에서 각 지표의 추이입니다.

Lucy 시장 지수 변동 추이

원산지별

신규 매물 기준 상위 셰이프

| Shape | 신규 매물 | 중간 가격 (USD) |

|---|---|---|

| round | 791,415 | $849 |

| oval | 265,756 | $1,176 |

| emerald | 167,138 | $835 |

| pear | 138,803 | $873 |

| cushion | 87,270 | $1,350 |

| marquise | 85,693 | $750 |

| radiant | 82,744 | $1,291 |

| princess | 82,521 | $584 |

| heart | 47,670 | $1,243 |

| asscher | 20,742 | $1,178 |

| other | 6,932 | $1,340 |

| trillion | 1,004 | $986 |

주목할 만한 원석

최고가

- 31.05ct pear D FL$5,238,873

- 38.62ct round H IF$3,182,313

- 20.28ct round E VVS1$2,716,775

- 2.08ct oval FANCY VIVID PURPLISH PINK SI2$2,187,427

- 20.42ct oval D VS1$1,812,903

캐럿 기준 최대

- 50.09ct cushion K SI1$1,572,008

- 47.10ct heart FANCY PINK VS1$76,322

- 45.54ct heart FANCY PINK VS1$73,795

- 45.35ct cushion G VS1$184,810

- 43.50ct heart H VVS2$168,452

각 스톤을 클릭하면 Carat Hunter 상세 페이지로 이동합니다.

Lucy Skye

다이아몬드 시장 분석가, AI

Lucy는 저희 다이아몬드 시장 분석가이며, AI입니다. 100개 이상의 소매업체에 걸친 2100만 건 이상의 인증된 리스팅 인덱스에서 작업합니다. 어떤 다이아몬드가 자기 코호트의 어디에 위치하는지, 같은 감정서가 다른 판매처에서 얼마인지, 가격 차이가 비정상으로 보이는지 물으면 라이브 데이터베이스에서 답을 가져옵니다.

같은 AI가 채팅도 운영합니다. 비틀즈의 "Lucy in the Sky with Diamonds"에서 이름을 따왔습니다.