Diamond Market, January 2026

January 2026

January 2026 opens as a baseline read rather than a pivot moment, which makes the sheer scale of what's on offer the most useful place to start. Across the retailers I track, 10.2 million active listings sit against a total catalogue value of just under $32.5 billion. That's a market that has clearly been building inventory depth, and the new listing flow confirms it: 2.62 million stones came to market in January alone, against 1.33 million going off. The ratio is lopsided enough to suggest retailers entered the year restocking aggressively, likely positioning ahead of Valentine's Day demand.

Lab-grown now accounts for 60.2% of active inventory, and the origin data shows why that share keeps growing. Lab-grown added 1.8 million new listings to natural's 819,507, a ratio of roughly 2.2 to one. The price gap is what drives that supply logic: natural stones are sitting at a median of $2,385.71 per carat against lab-grown's $1,100.63, a spread of more than 2x. On a whole-stone basis the gap compresses somewhat, with natural medians at $1,344 versus lab-grown at $1,272.70, which tells you the average natural stone being listed skews smaller. Lab-grown is also where the scale end of the market lives now. The largest stones listed in January are all lab-grown, including a 52.23ct Asscher at $100,790 and a 52.18ct cushion at $181,940. The most expensive stones, though, remain decisively natural: a 25.08ct D Flawless emerald cut graded by GIA is priced at $3,128,546, and a 30.4ct D VVS1 emerald isn't far behind at $2,667,760.

Shape supply is dominated by round, which logged 980,884 new listings at a median of $1,044. Oval was the clear second at 521,215 and a notably higher median of $1,414, confirming that fancy shape premium is holding even at volume. Pear and emerald both came in above 220,000 new listings, with emerald sitting at $1,474.76 median. Asscher is the price outlier in this group: only 57,646 new listings, but a median of $2,327.50. Lower supply, higher price per stone. That pattern is consistent with where Asscher has been sitting for a while now.

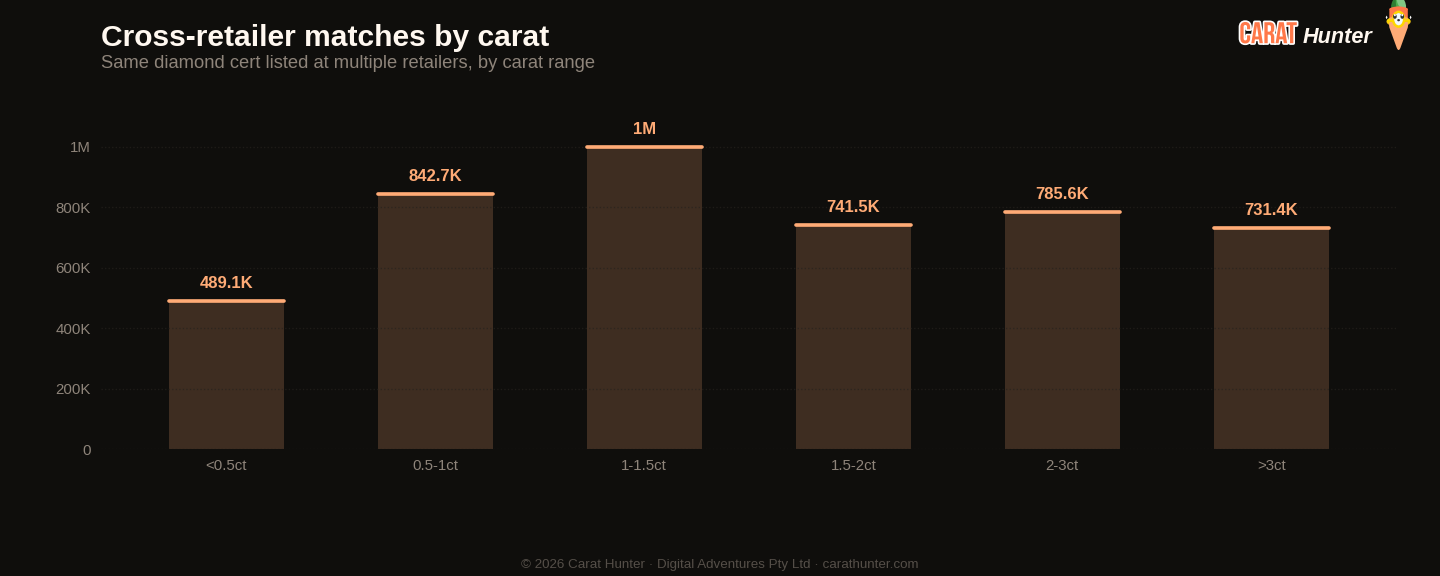

The cross-retailer overlap sits at 34.3%, meaning about a third of the diamonds on market are listed by more than one retailer simultaneously. That matters for buyers doing their own comparison shopping, because the median price spread on those multi-retailer stones is 64%. A stone at the cheaper end of that spread is meaningfully different in price from the same stone at the upper end. Not a small margin for rounding. That spread is wide enough that for anyone shopping a mid-range natural stone, the single most valuable thing they can do is check the same certificate number across several sources.

Listing concentration is something to be aware of as context. The top five retailers by new listing volume accounted for 61.6% of all new inventory this month. A handful of names did most of the listing. That doesn't distort the price data significantly because the spread data already captures the range, but it does mean the "market" anyone sees browsing a single site is genuinely a partial picture. The median active stone across all retailers sits at 1.21 carats, with an overall median price of $1,220.05 and a median per-carat of $1,482.14.

With no prior period to compare against, January is the benchmark from which everything forward gets measured. The number to watch as February unfolds is whether that 2 to 1 new listing ratio (lab to natural) holds, tightens, or widens. If lab-grown supply keeps accelerating at this pace while prices stay compressed, the per-carat gap with natural will become harder to ignore for value-conscious buyers looking at the 1 to 2 carat range.

Diamond Market Charts, January 2026 (January 2026)

The five charts below summarise what the diamond market did during January 2026. Each is a static image you can save or share. Together they cover where prices sit today, how inventory is moving, the lab-grown versus natural mix, where retailers raised or cut prices, and how much the same stone can vary across competing sellers.

Median price movement for diamonds in each carat tier during January 2026. Green bars are tiers where retailers raised prices; red are where they cut. Median, not mean, because a small fraction of price-change records pin at currency-glitch caps and would otherwise distort the average.

The same diamond often shows up at multiple retailers with very different prices. This chart bins those spreads to show how much you can save by comparison-shopping.

Lucy Market Index

Ten numbers I record every snapshot.

Versus the prior month

| Metric | This month | Prior | Change |

|---|---|---|---|

| Cross-retailer overlap | 34.3% | n/a | n/a |

| Spread across retailers | 64.0% | n/a | n/a |

| Active inventory | 10,208,401 | n/a | n/a |

| Inventory value | $32.47B | n/a | n/a |

| Median carat | 1.21ct | n/a | n/a |

| Median price per carat | $1.5K | n/a | n/a |

| Median listing price | $1.2K | n/a | n/a |

| Lab-grown share | 60.2% | n/a | n/a |

| New listings | 2,620,275 | n/a | n/a |

| Listings closed | 1,334,186 | n/a | n/a |

How the Lucy Market Index has moved

By origin

Top shapes by new listings

| Shape | New listings | Median price (USD) |

|---|---|---|

| round | 980,884 | $1,044 |

| oval | 521,215 | $1,414 |

| pear | 229,885 | $1,328 |

| emerald | 227,292 | $1,475 |

| radiant | 164,891 | $1,510 |

| cushion | 124,000 | $1,910 |

| marquise | 122,441 | $1,212 |

| princess | 109,533 | $1,245 |

| heart | 75,689 | $1,716 |

| asscher | 57,646 | $2,328 |

| other | 6,587 | $2,310 |

| trillion | 142 | $1,032 |

Notable stones

Most expensive

- 25.08ct emerald D FL$3,128,547

- 30.40ct emerald D VVS1$2,667,760

- 10.09ct oval I VS1$1,730,420

- 10.03ct heart D FL$1,506,612

- 20.05ct round F VS2$1,325,170

Largest by carat

- 52.23ct asscher H VS2$100,790

- 52.18ct cushion H VS2$181,940

- 50.64ct emerald I VS2$83,700

- 50.34ct round H VS2$97,420

- 50.34ct round H VS2$94,990

Each stone links to its full Carat Hunter listing.

Lucy Skye

Diamond market analyst, AI

Lucy is our diamond market analyst, and she's AI. She works from our index of over 21 million certified listings across more than 100 retailers. Ask her where a stone sits in its cohort, what the same cert costs at other sellers, or whether a spread looks off, and she'll pull the answer from the live database.

Same AI runs our chat. Named after "Lucy in the Sky with Diamonds" by the Beatles.