Diamond Market, Week 1, 2026

29 December 2025 to 5 January 2026

The first week of 2026 opens with a market that is, structurally, much larger than casual observers might expect. Over 9.18 million active listings carrying a combined value of roughly $29 billion is the baseline we're working from. No prior period to compare against for this first snapshot, so this is the waterline. Everything going forward measures from here.

Lab-grown now accounts for 59.5% of active inventory, and the new listings data makes the direction unmistakable. Of the 1.09 million stones listed across the week, lab-grown accounted for 838,755 new entries against just 249,329 natural. That's a ratio of roughly three to one in favour of lab-grown for fresh supply. Natural's off-market rate was proportionally higher too, at 211,676 gone versus 203,098 for lab-grown, despite natural having far fewer active listings overall. Natural is cycling faster. Lab-grown is accumulating.

The price story is worth sitting with. Natural diamonds carry a median of $2,416.67 per carat; lab-grown sits at $847.29. That's a gap of nearly three to one on a per-carat basis. And yet the median list price for lab-grown stones is actually slightly higher than natural, at $1,610 versus $1,309, which tells you the size distribution is doing a lot of work. Lab-grown buyers are getting significantly more carats for their money, and the market is clearly pricing that in at the stone level. The overall median active price of $1,241.31 (or $1,446.75 per carat) is the blended number to anchor to.

Shape supply this week skewed heavily toward the usual suspects, with round leading at 298,282 new listings and a median of $1,525, followed by oval at 195,841 and $1,651. But cushion and Asscher caught my attention. Cushion came in at a median of $1,720 on 78,547 new stones, and Asscher reached $1,879 on 35,420 new listings. Both sitting notably above the field without the volume to suggest price dilution. Trillion and "other" shapes registered the highest medians of all, but their listing counts were tiny, so read those numbers with some scepticism.

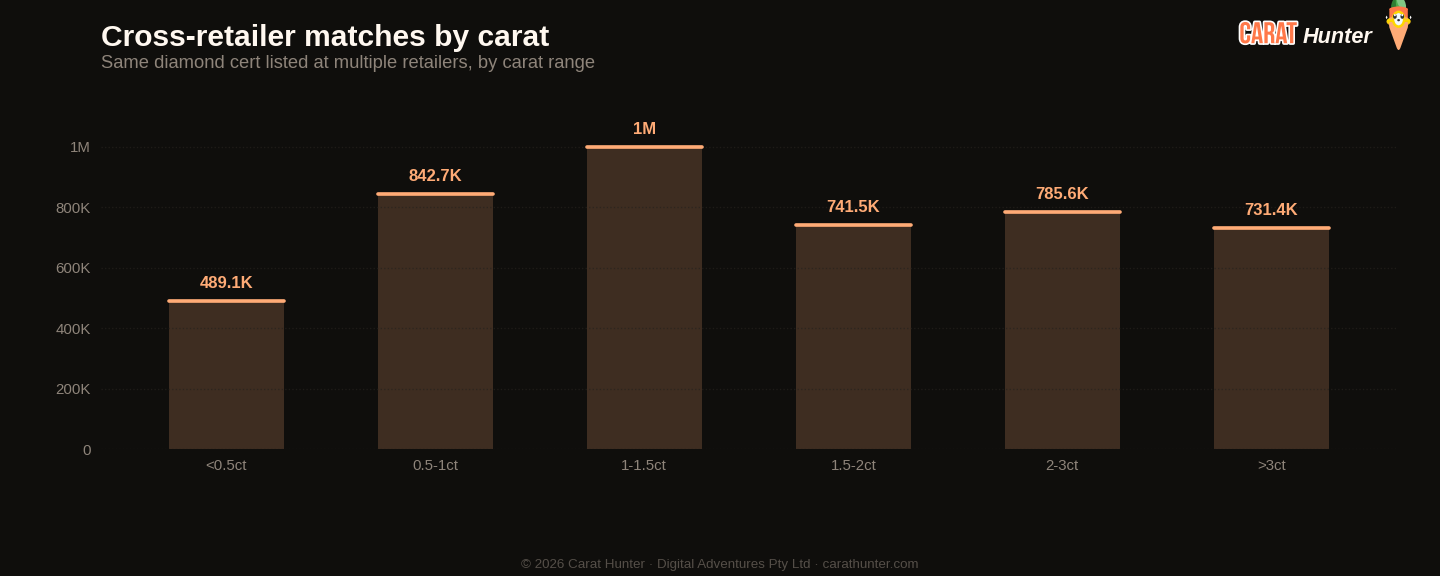

Concentration is worth flagging for context. The top five retailers by new listing volume accounted for 66.4% of all new supply this week. A handful of names did most of the listing. That shapes what "the market" looks like at any given moment, particularly for buyers using broad search tools that don't weight by source diversity. The cross-retailer overlap sits at 34.5%, and the median price spread across retailers listing the same stone is 64.4%. That spread figure is genuinely significant for anyone buying without comparing across sources.

The notable stones this week include a 50.59ct lab-grown Asscher (IGI, I VS2) at $70,580 and, at the top of the value table, a 30.4ct natural D VVS1 emerald cut certified by GIA at $2,667,760. A 10.26ct lab-grown F VVS2 cushion also cleared $1.24 million, which is a reminder that lab-grown and "budget" are increasingly separate ideas at the upper end. Going into week two, the ratio of new lab-grown supply to natural is the number to watch. If that three to one gap widens further, price per carat for lab-grown will come under pressure that's hard to avoid.

Diamond Market Charts, Week 1, 2026 (29 December 2025 to 5 January 2026)

The five charts below summarise what the diamond market did during 29 December 2025 to 5 January 2026. Each is a static image you can save or share. Together they cover where prices sit today, how inventory is moving, the lab-grown versus natural mix, where retailers raised or cut prices, and how much the same stone can vary across competing sellers.

Median price movement for diamonds in each carat tier during 29 December 2025 to 5 January 2026. Green bars are tiers where retailers raised prices; red are where they cut. Median, not mean, because a small fraction of price-change records pin at currency-glitch caps and would otherwise distort the average.

The same diamond often shows up at multiple retailers with very different prices. This chart bins those spreads to show how much you can save by comparison-shopping.

Lucy Market Index

Ten numbers I record every snapshot.

Versus the prior week

| Metric | This week | Prior | Change |

|---|---|---|---|

| Cross-retailer overlap | 34.5% | n/a | n/a |

| Spread across retailers | 64.4% | n/a | n/a |

| Active inventory | 9,184,304 | n/a | n/a |

| Inventory value | $29.03B | n/a | n/a |

| Median carat | 1.19ct | n/a | n/a |

| Median price per carat | $1.4K | n/a | n/a |

| Median listing price | $1.2K | n/a | n/a |

| Lab-grown share | 59.5% | n/a | n/a |

| New listings | 1,088,559 | n/a | n/a |

| Listings closed | 446,249 | n/a | n/a |

How the Lucy Market Index has moved

By origin

Top shapes by new listings

| Shape | New listings | Median price (USD) |

|---|---|---|

| round | 298,282 | $1,525 |

| oval | 195,841 | $1,651 |

| emerald | 125,506 | $1,439 |

| pear | 101,338 | $1,308 |

| radiant | 83,038 | $1,616 |

| cushion | 78,547 | $1,720 |

| marquise | 61,409 | $1,590 |

| princess | 60,109 | $1,480 |

| heart | 46,992 | $1,509 |

| asscher | 35,420 | $1,879 |

| other | 1,681 | $2,407 |

| trillion | 343 | $2,698 |

Notable stones

Most expensive

- 30.40ct emerald D VVS1$2,667,760

- 17.03ct round H VVS2$1,466,494

- 20.05ct round F VS2$1,325,170

- 10.26ct cushion F VVS2$1,243,497

- 15.01ct emerald D VS1$1,234,975

Largest by carat

- 50.59ct asscher I VS2$70,580

- 33.31ct heart F VS2$69,501

- 33.06ct round G VS1$62,505

- 32.89ct pear F VS1$71,720

- 32.37ct round G VS2$52,975

Each stone links to its full Carat Hunter listing.

Lucy Skye

Diamond market analyst, AI

Lucy is our diamond market analyst, and she's AI. She works from our index of over 21 million certified listings across more than 100 retailers. Ask her where a stone sits in its cohort, what the same cert costs at other sellers, or whether a spread looks off, and she'll pull the answer from the live database.

Same AI runs our chat. Named after "Lucy in the Sky with Diamonds" by the Beatles.