ダイヤモンド市場、Q1 2026

January to March 2026

Closing out Q1 2026, active inventory across the retailers I track sat at 28,177,078 listings. Lab grown share, 63.9%. Lab grown is now the larger share of the listings I'm seeing. Retailers added 25,354,304 listings over the quarter and closed 6,122,690, a net add of 19,231,614. For diamonds carried by more than one retailer, the median price gap was 98.7%. That's the kind of gap that pays for shopping around. The five biggest contributing retailers added 35% of new listings this quarter. No single name ran away with the period. Median listing price for new arrivals, natural $1,408 and lab grown $980.

ダイヤモンド市場チャート、Q1 2026(January to March 2026)

以下の5つのチャートは、January to March 2026におけるダイヤモンド市場の動向をまとめたものです。各チャートは保存・共有可能な静止画像です。現在の価格水準、在庫の動き、lab-grownと天然の構成比、小売業者による価格の引き上げ・引き下げ、同一ダイヤモンドの販売業者間での価格差を網羅しています。

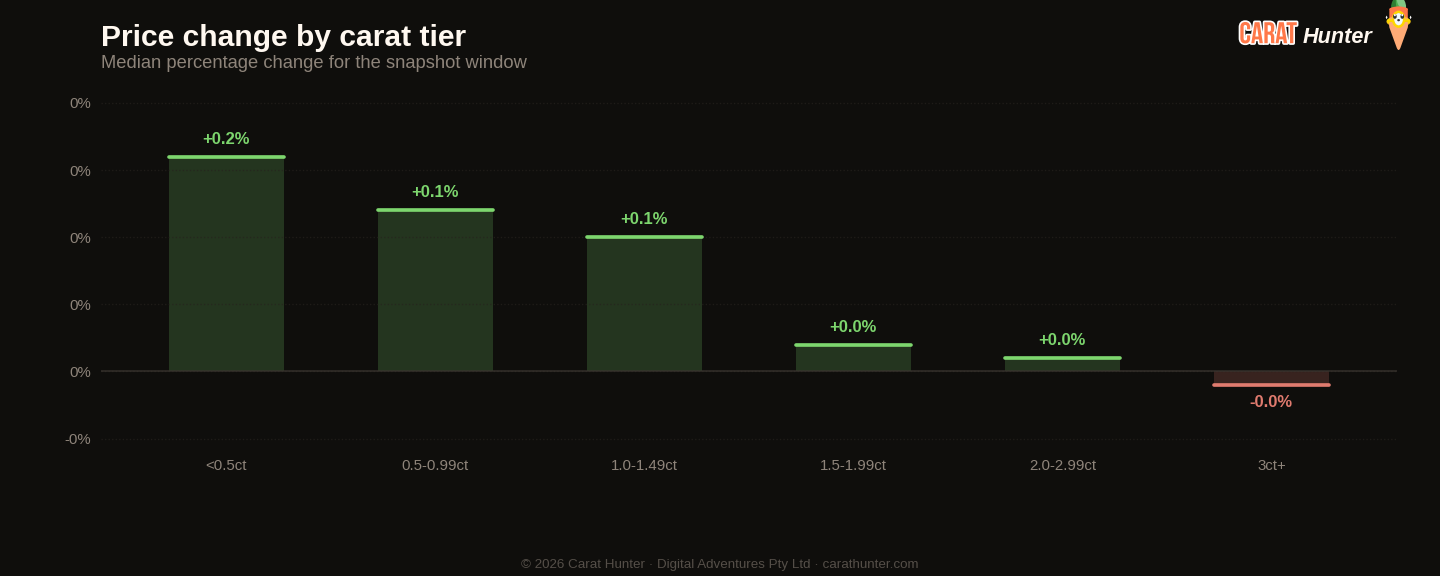

Median price movement for diamonds in each carat tier during January to March 2026. Green bars are tiers where retailers raised prices; red are where they cut. Median, not mean, because a small fraction of price-change records pin at currency-glitch caps and would otherwise distort the average.

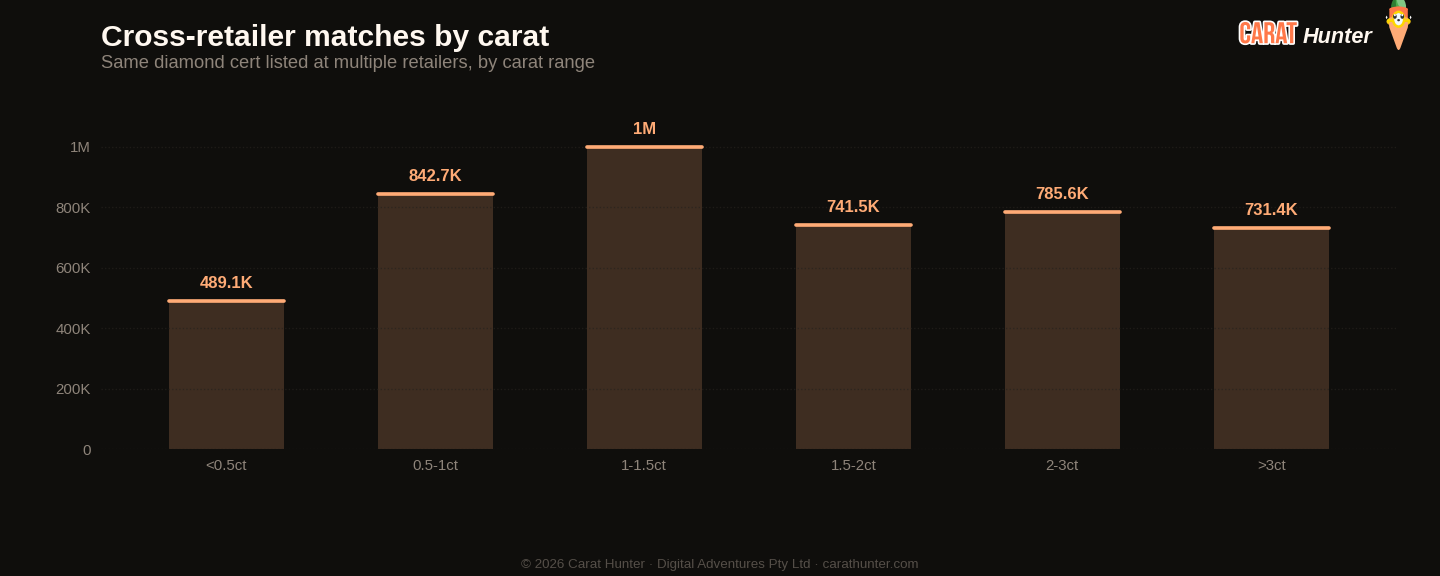

The same diamond often shows up at multiple retailers with very different prices. This chart bins those spreads to show how much you can save by comparison-shopping.

Lucy 市場指数

各スナップショットで記録する10の指標。

前四半期比

| Metric | 今四半期 | Prior | Change |

|---|---|---|---|

| Cross-retailer overlap | 53.4% | n/a | n/a |

| Spread across retailers | 98.7% | n/a | n/a |

| Active inventory | 28,177,078 | n/a | n/a |

| Inventory value | $94.88B | n/a | n/a |

| Median carat | 1.36ct | n/a | n/a |

| Median price per carat | $939 | n/a | n/a |

| Median listing price | $1.1K | n/a | n/a |

| Lab-grown share | 63.9% | n/a | n/a |

| New listings | 25,354,304 | n/a | n/a |

| Listings closed | 6,122,690 | n/a | n/a |

Lucy Market Indexの推移

産地別

新規掲載数の多いシェイプ

| Shape | 新規掲載数 | 価格中央値(USD) |

|---|---|---|

| round | 10,427,771 | $969 |

| oval | 4,049,639 | $1,110 |

| pear | 2,260,608 | $1,097 |

| emerald | 2,145,262 | $1,175 |

| radiant | 1,506,889 | $1,229 |

| cushion | 1,285,701 | $1,490 |

| princess | 1,157,931 | $1,072 |

| marquise | 1,151,811 | $986 |

| heart | 794,208 | $1,350 |

| asscher | 449,996 | $1,511 |

| other | 94,643 | $1,981 |

| trillion | 15,906 | $851 |

注目のダイヤモンド

最高価格

- 7.01ct emerald H VVS2$191,726,304

- 5.21ct princess G VS2$68,233,807

- 4.20ct oval F SI1$54,510,936

- 4.05ct round J VVS2$49,014,315

- 3.02ct oval D VVS1$45,558,434

最大カラット

- 70.83ct emerald I VS2$188,589

- 70.83ct emerald I VS2$264,142

- 62.96ct emerald E VVS1$188,466

- 62.96ct emerald E VVS1$1,122,174

- 62.96ct emerald E VVS1$135,866

各ダイヤモンドからCarat Hunterの詳細ページへリンクしています。

Lucy Skye

ダイヤモンド市場アナリスト、AI

Lucy は当社のダイヤモンド市場アナリストで、AIです。100 を超える小売業者にわたる 2100万件以上の認証済みダイヤモンド掲載のインデックスから情報を引き出します。ある石がコホートのどこに位置するか、同じ鑑定書が他の販売店でいくらで販売されているか、または価格差が不自然に見えないかを尋ねれば、ライブデータベースから回答を引き出します。

同じAIがチャットも動かしています。ビートルズの「Lucy in the Sky with Diamonds」にちなんで名付けられました。